- Your Money & Your Life

- Posts

- The solution to the housing crisis + My top 5 money mistakes

The solution to the housing crisis + My top 5 money mistakes

My Money Digest - 18 July 2025

David Koch

July 18, 2025

Hi everyone from beautiful Albany.

Libby and I are visiting the grandkids in WA this week and spending a few days in Albany down on the Great Southern coast. Beautiful area and home to an incredible ANZAC museum.

The grandkids have been busting to bring us down here as Albany was where the first convoy of troops left to train in Egypt before fighting in the Gallipoli Campaign.

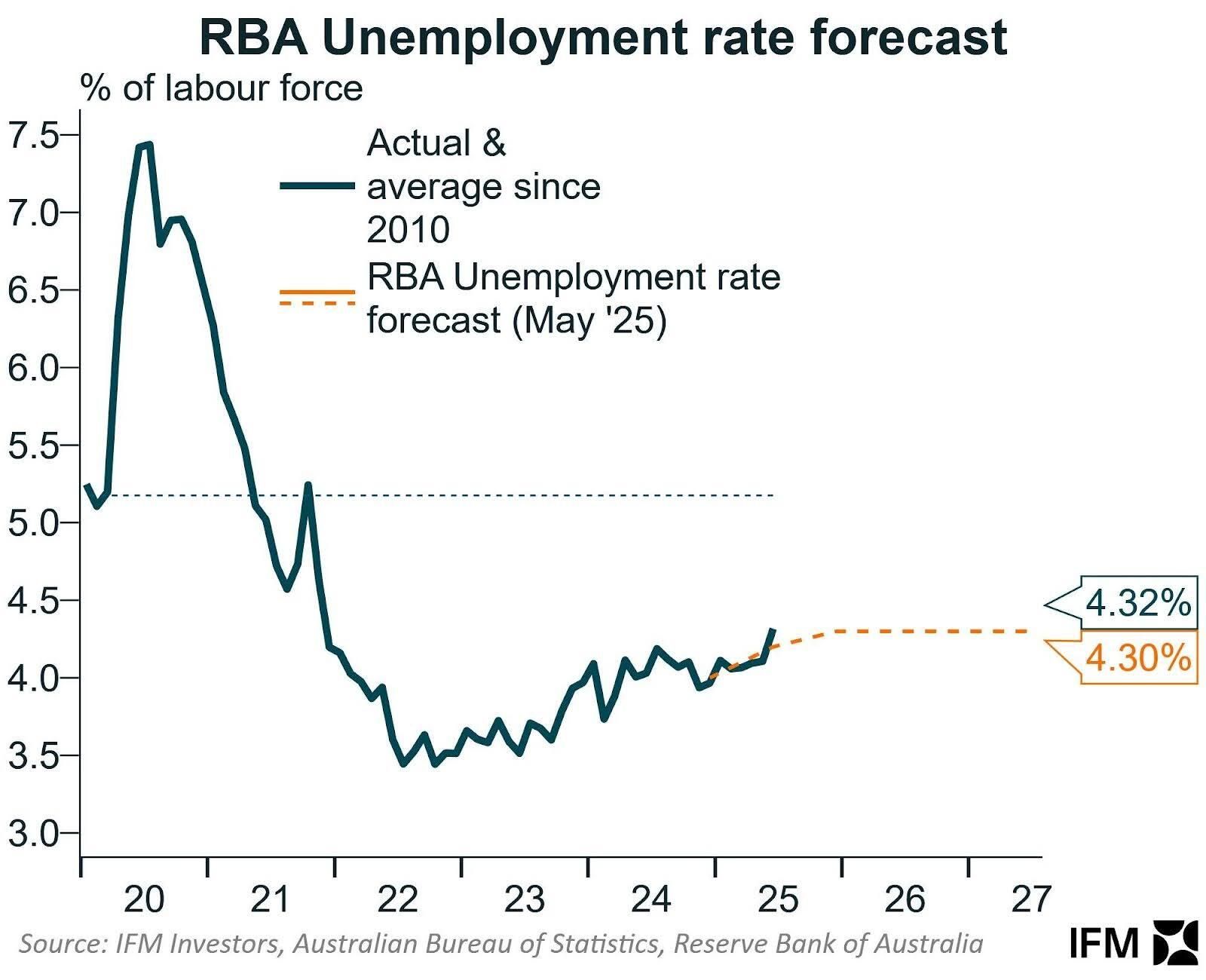

On the finance front, the Reserve Bank looks to have received two bits of economic data- building costs and unemployment - this week which points to a rate cut next month. All the RBA needs is a good CPI figure at the end of the month to make a cut certain.

In this week’s newsletter:

Rate cut indicator 1: Weakening jobs market.

Rate cut indicator 2: Construction costs.

Do we need to think outside the square to reduce building costs?

Understanding profit season: What it means for your shares.

Top 5 money mistakes.

Building financial bliss … as well as wedding bliss.

Credit card fine print.

How we rate in work-life balance.

Rate cut indicator 1: Weakening jobs market

Last week I discussed the Reserve Bank’s decision to keep official interest rates on hold. In a nutshell, the RBA Governor Michele Bullock wants to wait for the June quarter CPI figures to be released on 31 July to see whether inflation is staying within the desired 2-3 per cent target band.

She is worried by building costs which seem to be staying stubbornly high and is wary of a tight labour market pushing up wages.

I’ll come to building costs next, but the jobs market showed distinct signs of weakening in the month of June, even though it was very solid in the first part of the quarter.

In June, only 2000 new jobs were added to the economy with the unemployment rate rising from 4.1 per cent in May to 4.3 per cent in June. For the June quarter, unemployment matched the RBA’s forecast 4.2 per cent.

History tells us that when the unemployment cycle turns down, it does so quickly - which would worry the RBA. The fact that unemployment in Australia’s two biggest states is higher than the national average is a bit concerning.

The NSW unemployment figure came in at 4.4 per cent and Victoria is 4.6 per cent.

In addition, the NAB quarterly business survey released yesterday shows that businesses are having an easier time hiring new employees.

Rate cut indicator 2: Construction costs

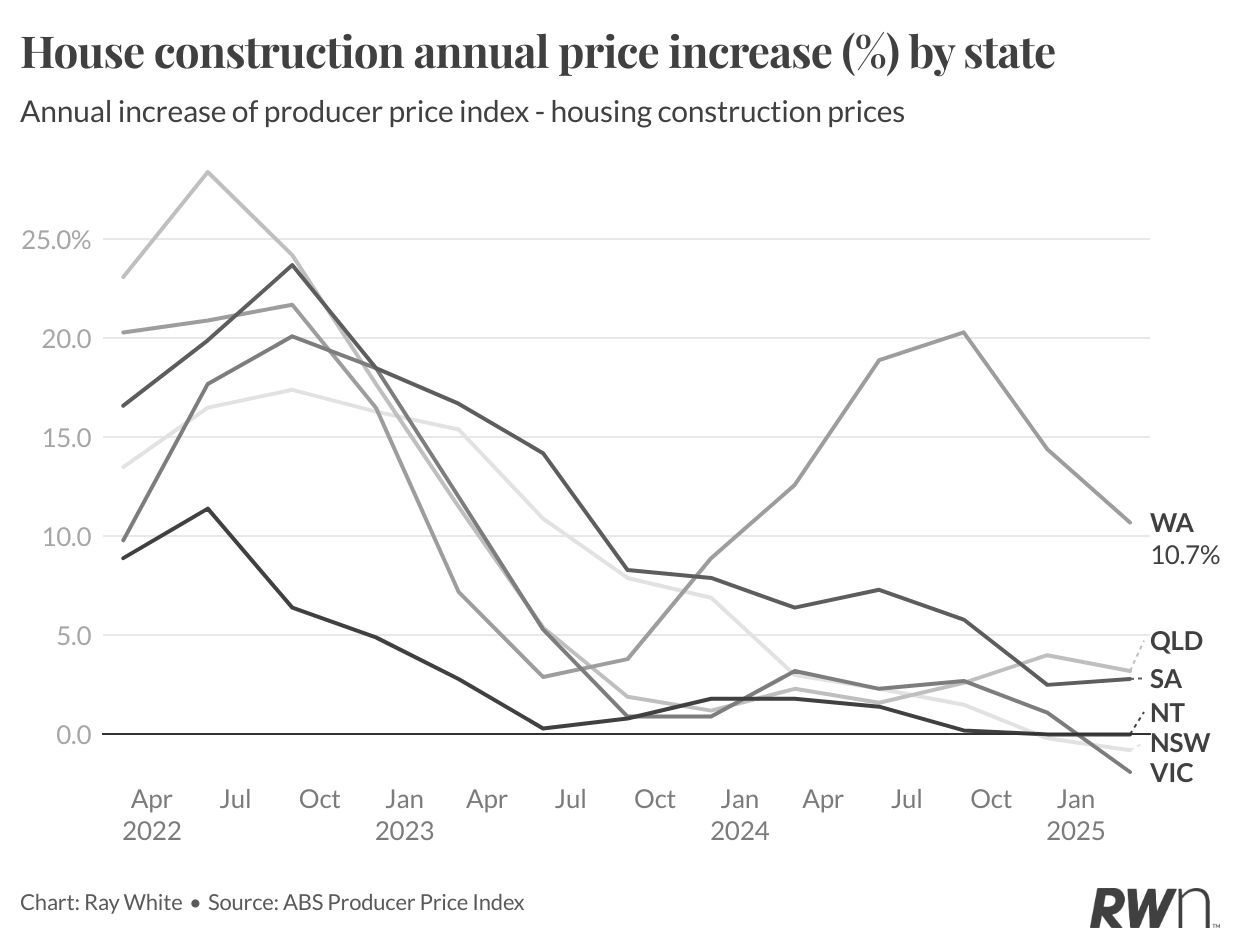

This week, Cotality’s latest Cordell Construction Cost Index showed construction costs picked up slightly to grow 0.5 per cent over the June quarter following a 0.4 per cent rise in the March quarter, which was the lowest quarterly increase since March 2010.

The rise was subdued but it seems Michele Bullock was right to worry that it could pick up speed slightly. The latest result is still half the long-term pre-pandemic average of about 1 per cent a quarter.

Over the year leading up to the end of June, construction costs increased by 2.9 per cent. This is within the RBA's target for inflation, but it's slightly higher than the 2.6 per cent increase expected for the year ending in June 2024.

So, construction costs have re-accelerated but the question is whether it’s enough to stop a rate cut at the end of the month?

With the cost of building a new home continuing to rise, the target of building 1.2 million new homes by July 2029 to ease housing affordability issues, is looking unachievable.

Builders are struggling with the shortage, and increasing cost of labour as workers are being lured away to higher paying jobs in public infrastructure projects (like transport and renewable energy projects) and that demand for jobs is likely to stay for a few more years.

Home builders have to pay higher wages to keep workers from going to infrastructure projects which, in turn, cuts into their profit margins. So, they have to lift their profits or go broke.

That is the issue facing the RBA decision for another rate cut. The problem with building costs boils down to the cost of labour. High costs have eroded builder margins and contributed to the housing affordability crisis.

Do we need to think outside the square when it comes to building costs?

While construction costs have dramatically slowed from their pandemic peaks of 17.8 per cent annual growth in December 2022, the damage it has done to housing affordability has been severe.

While building costs have declined significantly in NSW and Victoria, they are still rising by 10 per cent in WA. This cost inflation has fundamentally altered housing construction economics, making traditional building methods increasingly unviable for affordable housing.

Nerida Conisbee, the chief economist at Ray White, has been looking for creative solutions to the housing crisis, focusing on reducing building costs.

According to Nerida, a major challenge in reducing costs is that Australia's housing construction industry has remained largely unchanged for decades, relying on site construction that is inherently inefficient. The traditional process requires coordinating multiple sub-contractors across numerous sites with varying conditions and logistical challenges.

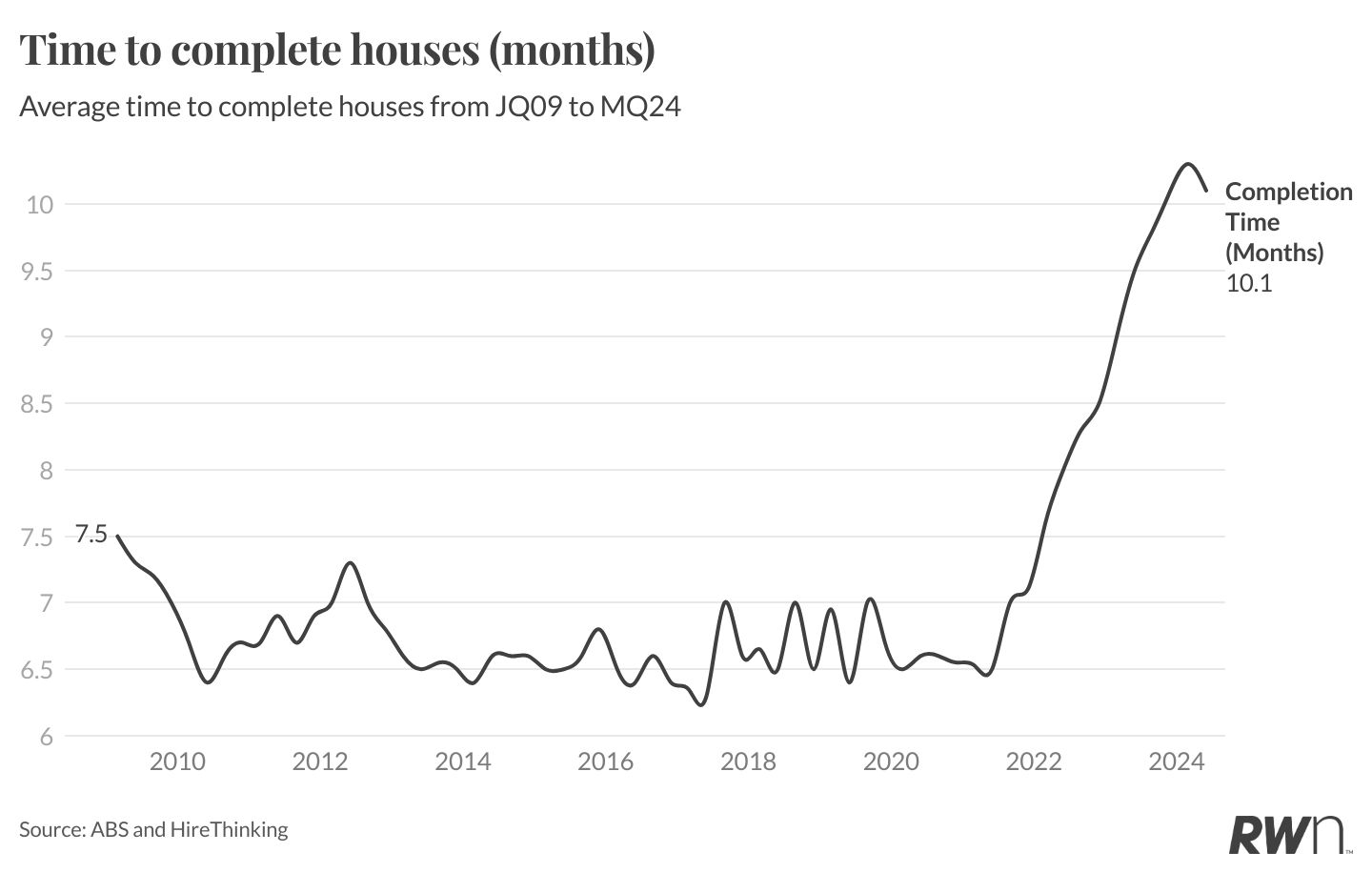

It has been further compounded by labour shortages. Master Builders Australia research has found that the industry requires 90,000 new workers to meet current demand - a shortage that would require 360,000 years of training if filled entirely through traditional apprenticeships.

Rising costs, inefficiencies in the way homes are built and labour shortages has meant that dwelling completion times have now reached historic highs. The average house now takes over 10 months to complete, compared to 6-7 months in normal conditions. Against this background, modular construction is now emerging as a way to increase efficiency in housing construction.

Modular construction can reduce building costs by 10-20 per cent, while cutting construction timeframes by up to 50 per cent compared to traditional methods. The fundamental reason for these savings is that a house is largely built in a factory rather than on a building site.

Factory-based construction eliminates weather delays, reduces material waste through precise manufacturing, and achieves economies of scale impossible on individual construction sites.

When components are manufactured in controlled environments, quality improves while labour costs decrease through more efficient deployment of skilled workers.

Rather than coordinating trades across multiple sites, modular construction consolidates activities in controlled environments where workflows can be optimised, materials managed efficiently, and quality assured through standardised processes.

Right now, the use of modular in building homes is growing but not dramatically so. The market has grown from $3.7 billion in 2018 to a projected $7.7 billion by 2030, representing a compound annual growth of 6.4 per cent.

Nerida is challenging the housing industry and governments to think differently in solving the housing crisis. And there is more innovation available.

LUYTEN's 3D printed multi-storey home in Melbourne completed construction in just five weeks, compared to the typical 8-11 months for traditional builds.

Amazon's $4,999 "snap-on" tiny home demonstrates how extreme standardisation can drive costs down dramatically.

For modular construction to achieve its potential, manufacturing capacity must expand significantly, requiring substantial investment in factory facilities.

In the 2025–26 Federal Budget, the Australian Government allocated $54 million to support the prefabricated and modular housing sector. Additionally, the government committed $120 million from the National Productivity Fund to incentivise states and territories to eliminate regulatory barriers hindering the adoption of modern construction methods, including modular and prefabricated building techniques.

Let's hope it achieves the desired result, and quickly.

Understanding profit season: What it means for your shares

For Australia's public companies, this is the moment of truth. The 2025 profit reporting season has started, and this is when companies on the ASX let the market know how much money they earned last year.

Reporting season is an exciting but sometimes stressful time for investors. It's when companies share the most detailed information about how they're doing and what they expect for the future.

This makes now a great time to properly assess potential investments, as well as evaluate any investment decisions you’ve made throughout the year. But it’s not always easy. Profit result announcements and annual reports are full of jargon, and things are not always as rosy as they appear on the outside.

Here’s what you need to know to cut through the noise.

Look at the bigger picture

Most investors reading a company’s annual report and financial statements are looking to glean enough information to decide whether the business is a good investment.

Unfortunately, there’s no magic calculation to tell you this. You need to assess a wide range of qualitative and quantitative information to form an opinion.

Successful investors take a long-term approach to this process.

While profitability and revenue growth are important factors, ask yourself whether these are sustainable over the next three to five years.

Are there internal or external risks that could impact the performance of the company? Does it have a competitive advantage in the marketplace? How much debt does it have? How much does it plan to take on? And how experienced and stable is the management team?

Always remember that it’s in a company’s interests to paint things in the best possible light, so assume the report is biased and then balance it with your own research and conclusions.

The financial statements

Public companies are required by law to comply with relevant accounting standards and list their financial statements with the Australian Securities and Investments Commission within three months of the end of their financial year.

The three main financial statements are:

The Statement of Comprehensive Income, detailing revenue, expenses and profit (or loss).

The Statement of Financial Position, which sets out the company’s assets, liabilities and equity.

The Statement of Cash Flows, which lists all cash transactions for the reporting period.

You may also hear these referred to as the Income Statement, Balance Sheet and Cash Flow Statement.

These are typically accompanied by a ream of explanatory notes, which can be helpful to shed light on how the accountants arrived at the final figures.

Key terms

These are some of the main accounting terms that every would-be-investor needs to be across. This isn’t an exhaustive list, and key terms will often vary depending on the specific business and industry you’re looking at, so do your homework.

Net Profit After Tax (NPAT) - A measure of how much money the company made after every single expense has been accounted for. While it’s commonly reported, it can be influenced by various accounting practices, so it’s not always a reliable indicator of overall performance.

Earnings Before Interest and Tax (EBIT) - Think of this as NPAT plus interest and ax charges. EBIT is helpful when comparing companies with different tax rates or debt levels.

Earnings Per Share (EPS) - The company’s profit is divided by the number of shares on issue.

Return on Equity (ROE) - The company’s profit is divided by shareholder equity (assets minus liabilities). This shows the rate of return investors get on the money they’ve invested.

When comparing key measures, be sure to look at industry peers and averages to get an idea of how a company is faring relative to the competition.

While reading financial statements and annual reports may seem like information overload, the more you do it the better you get at understanding of them, and the better you’ll understand the business.

Your Money & Your Life premieres on the Seven Network today

A brand new season of Your Money & Your Life is premiering today on the Seven Network. This is my personal finance TV show aimed at helping people save, spend, invest and manage their money better.

I want to help everyday Australians keep more money for themselves during these tough times of inflation and interest rate hikes. I have loads of tips for how you can ease the strain on your household budget, and get on top of your finances.

So check it out next time you’re looking for something to watch!

Top 5 money mistakes

I was speaking at an investment seminar a couple of weeks ago and they asked me for my top five money mistakes.

Interesting question. These were the five we rattled off:

Living on credit and spending beyond your means.

If you can’t pay cash or can’t pay off your credit card every month, you can’t afford it. Minimise the credit in your life and you’ll be minimising the financial stress and risk of serious problems.

Under, or not, insuring your valuables.

Make sure all your valuables (car, home and contents, health) are insured to their full value. Always keep your eye out for better deals and never automatically renew a policy without checking around first, but don’t water down actual coverage.

Repaying the bare minimum.

Don’t get caught in the minimum payment trap on your credit card. The minimum doesn’t even cover the interest so it will compound for months to come and end up being a huge bill.

Buying a new car.

New cars fall in value by a third when you drive out of the dealership. Shop around the auctions, secondhand dealers and internet sites to grab an “as new” used car. There are some good quality bargains out there!

Making your budget too tight.

It’s good to budget and save, but make sure (when possible) to stash away a bit of extra cash to dip into for emergencies, occasional treats, or that rainy day.

Building financial bliss … as well as wedded bliss

When a couple decides to get hitched, chances are neither party is basing their decision on how financially compatible they are together.

At least I hope that’s not the case … I’m a romantic at heart.

But once the dregs of the wedding cake have finally been thrown away and the honeymoon snaps are safely in their frames, how you deal with money as a couple becomes a critical consideration.

Financial incompatibility and pressure is one of the top factors behind couples divorcing in Australia every year, so it’s a good idea to talk about money well before the big day.

To guide the conversation, here are five financial matters to get sorted before walking down the aisle.

Be open about money

If you don’t form good habits early on in a relationship then the bad ones will stick with you. This means you’ve got to start out being open and honest about your financial situation as soon as things get serious.

You’ve already made the decision to spend the rest of your life together, so there should be enough trust to share things like your salary and any dirty debts you’ve picked up along the way.

Otherwise, that hidden income or concealed credit card will cause problems when it’s inevitably discovered.

Understand each other’s values and goals

It’s important for each person to understand what the other wants to achieve financially, both in the relationship and for themselves.

Don’t expect to be 100 per cent aligned on everything; there’s no right or wrong answer, and words like security, lifestyle and comfort mean different things to different people.

But once you’re on the same page, it makes managing money so much easier, from everyday issues like choosing a restaurant to tough decisions like how much to spend on a house or where to send the kids to school.

Line up spending habits

If one person is squirrelling away every spare dollar while the other is consistently blowing their wages on the latest ‘must haves’, then sooner or later there will be conflict.

This can be avoided by making sure your spending habits are compatible. A budget will help here, as will understanding each other’s goals.

I’ve met so many couples who, through being disciplined with their money and working towards the same goals, have ended up with more wealth than those who earn three or four times as much but spend the lot.

The joint account

While it’s certainly not essential to have joint banking accounts, they can make the process of managing money simpler, more transparent and fair. Think splitting bills, buying groceries and paying the rent or mortgage.

And if you spend less time arguing about money, then you can spend more time enjoying your relationship.

To make a joint account work, a good option is to set up three accounts: yours, theirs and the joint account, with wages deposited into your individual accounts.

Then look at what you both earn and set up an automatic transfer for a certain percentage (to keep things fair) of each wage into the joint account each month.

If only one partner earns, you'll need to work backward. Deposit the entire wage into the joint account first, then transfer money into each individual account.

Don’t be financially ignorant

For two people to jointly manage their finances, each partner must have a basic understanding of money.

Start by opening your eyes and ears to financial news - daily newspapers, television, radio and books on money can all provide enormous help. For more complex matters, it can be extremely helpful to see a financial planner together.

By squaring up your financial relationship before tying the knot, you can avoid conflict later and build a brighter future together.

Credit card fine print tricks

Before you commit to a new credit card, read the fine print and understand the interest charges. Dig out the terms and conditions booklet for any existing cards; if it found its way to the recycling years ago, contact your credit card provider for a new one.

Here’s what you need to look out for:

Trick: Backdated interest

If you pay your credit card bill late, or don’t pay it in full, most companies will charge daily interest from the date of your original transactions. So, if you are just one day late paying the bill you could be charged daily interest on all transactions up to 55 days ago.

Trick: No benefit for partial repayments

Most companies don’t give you any credit for paying off part of your bill on time - they will still backdate interest on the full amount of your purchases. So just say you paid $900 of a $1000 credit card bill, you would still be charged interest on the entire $1000.

Trick: No interest-free period for new transactions

If you don’t pay your credit card bill in full and on time you can kiss your next interest-free period goodbye. Most credit card providers will charge interest on new purchases, instead of giving you a 55-day interest-free period, until you pay off your debt in full.

The best way to avoid interest charges is to be disciplined and pay off your credit card debt in full every month. Keep track of when your bill is due to avoid costly late payment fees and additional interest charges.

If you are one of those people who just can’t seem to pay their bill off every month, you need to pay close attention to these tricks of the credit card trade. Add up just how much the convenience of credit is costing you. Is it worth it?

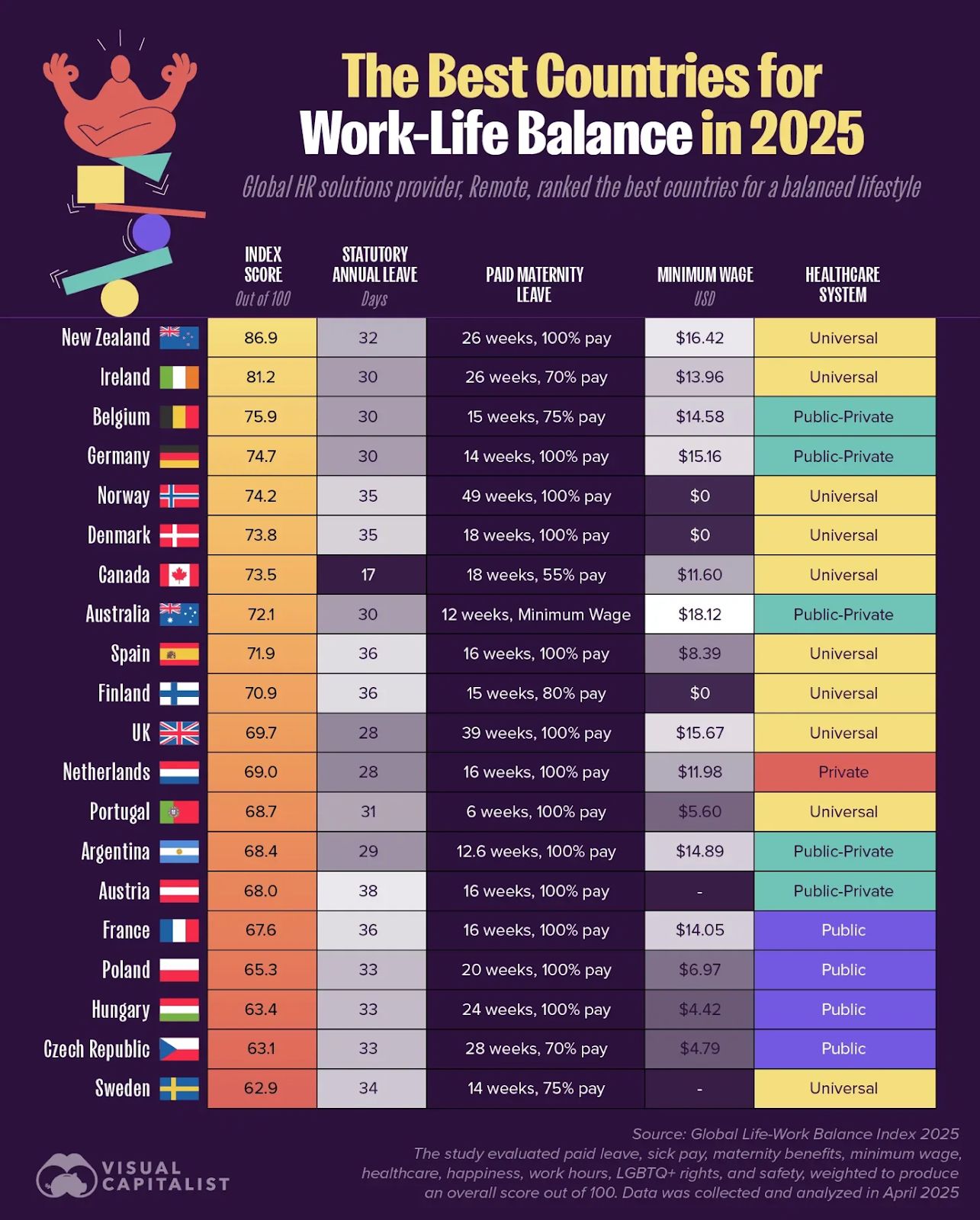

How we rate in work-life balance

Over the last few weeks there have been a string of global studies rating our capital cities as some of the most liveable in the world. There is no doubt we are lucky to live in this country and we should never forget it.

This is another interesting study which ranks us highly when it comes to achieving work-life balance: