- Your Money & Your Life

- Posts

- Rate hikes and property + How to save $50 a week on fuel

Rate hikes and property + How to save $50 a week on fuel

My Money Digest - 24 April 2026

David Koch

April 24, 2026

Hi everyone,

Enjoy the upcoming ANZAC long weekend - a time to pause and reflect on how fortunate we are today because of the sacrifices of those who fought for us.

We’ve had a spate of public holidays in April and it’s been a nice reset, but it’s time to focus on some major economic decisions coming in May - the Reserve Bank board meeting and the federal Budget.

I’ll be unpacking both here.

This week’s newsletter:

Rising rates deplete borrowing power.

The Australian dream of owning a home isn’t lost ... it’s just different.

Expert views on what to do now across investment markets.

Why property markets are becoming fragile.

5% Deposit Scheme ignites property values under the cap.

Smart ways to save $50 a week on fuel.

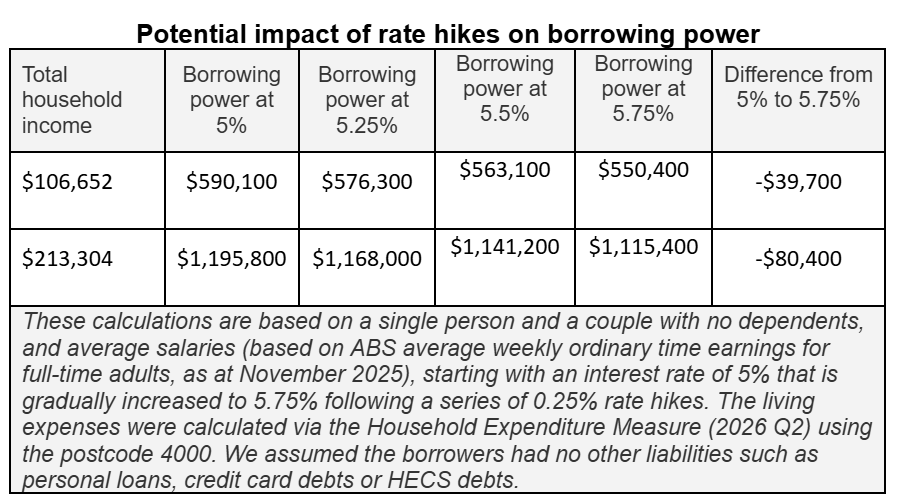

Rising rates deplete borrowing power

With the next Reserve Bank of Australia Board meeting scheduled for the week after next, financial markets are indicating a 60–70 per cent chance of another 0.25 per cent interest rate increase.

I hope not as it would the third straight rate rise, plus the rise in petrol prices, which could potentially crush Australian household budgets.

But rate rises don’t just mean higher monthly mortgage repayments. They also mean reduced borrowing power.

Aspiring buyers may have to save more, or rein in their budget, as cash rate hikes put the squeeze on borrowing power.

New figures from Compare the Market show that maximum loan sizes for average borrowers have shrunk by tens of thousands of dollars.

The comparison website analysed a single borrower on an average wage of $106,652, as well as a couple on average salaries with no dependants.

The single borrower’s borrowing power could be up to $39,700 lower than it was just a few months ago if a third consecutive rate hike is confirmed in May.

The couple’s borrowing power would fall by around $80,400 after three 0.25 per cent rate increases.

Source: Compare the Market

The rapid rise in interest rates has once again highlighted why mortgage stress testing matters.

Not long ago, we were enjoying rate cuts and looking forward to more, but the picture has completely changed this year - now it looks like much of that mortgage relief will be reversed.

Maximum loan size limits exist to stop people taking out silly-sized loans they’ll struggle to service.

And as this research shows, it doesn’t take many rate hikes for that maximum loan amount to fall away very quickly.

That’s why I always encourage people to do their own mortgage stress testing and work out what’s realistically within their budget.

You’ve got to ask yourself: what happens if you have kids, lose a job, or face a financial emergency? What loan would you still feel comfortable repaying in those situations?

The big question right now is simple - could you still afford your repayments if interest rates were to rise another two or three times?

As a rule of thumb, you really don’t want to be spending much more than a third of your

income on repayments. That way, you’ve still got room for everyday bills, unexpected costs, and a bit left over for savings and peace of mind.

Tighter borrowing budgets would likely have a cooling effect on some of the country’s overheated property markets ... potentially good news for savvy buyers.

People may not be able to borrow as much as they once could, but that doesn’t necessarily hurt their chances of buying a home, particularly if they were already in a good position to do so.

Everyone is in the same boat, so even if your buying budget has shrunk, it’s likely the

buyers you’re competing with are facing the same challenge.

But buyers shouldn’t be banking on rapid rate cuts to save the day. The safer approach is to plan as if today’s conditions are here for a while.

Focus on what you can comfortably afford now. A good broker will be able to help you run the numbers and look for a competitive rate that can help keep your repayments manageable too.

If you're really in a great position to buy, have a healthy deposit saved, and know what you’re looking for, then higher interest rates needn’t stop you buying a home. Cooler conditions might even work in your favour.

The Australian dream isn’t what it used to be, but it’s not lost either

I came across a fascinating research report from Ray White economist Atom Gi Tian during the week, which shows that homeownership remains within reach for most Australians. Atom also shows that different housing policies across countries can be just as effective.

The OECD’s latest data puts Australia’s combined homeownership rate at 62.7 per cent, steady for over a decade and just below the OECD average of 70.1 per cent. What has changed is not whether Australians own homes, but how - and more importantly, at what cost.

As house prices have climbed, the path from renter to mortgaged owner to outright owner has lengthened significantly. People are entering the market later, borrowing more relative to income, and carrying debt further into middle age. The dream is still alive, but the quarter-acre block has shrunk to an apartment, and the finish line keeps moving.

This is not a uniquely Australian experience. Around the world, countries are grappling with the same question: what does housing security look like when the old model no longer works? The answers, it turns out, are more varied and more instructive than the local debate suggests.

Among OECD countries, Romania (91.7 per cent) and Croatia (84.3 per cent) have the highest share of households who own outright. But their high rates trace back to a single policy event: the mass transfer of state housing stock to sitting tenants in the early 1990s. People own their homes free and clear, which delivers real security of tenure.

The downside is that the rental market never developed depth, so labour mobility is limited (it’s hard to move for a job when renting is expensive and scarce), housing quality is uneven, and property is often illiquid or difficult to renovate. The geopolitical context these countries found themselves in is hardly easy to replicate in Australia today.

On the other side of the spectrum sits the most direct alternative to the Australian Dream. Western European countries such as Switzerland, the Netherlands, Denmark and Germany have built housing systems around renting as a legitimate, stable long-term choice, not a stepping stone to ownership.

In Switzerland, where around 61.1 per cent of households rent, and Germany, at 55.4 per cent, renting is the dominant tenure. This reflects strong tenant protection laws, professionally managed rental stock, historically rent-controlled urban housing, and a deliberate post-war policy decision not to subsidise owner-occupation to the same extent as countries like the UK or the US.

Japan offers the most radical alternative. Residential buildings depreciate to near zero within 30 years, stripping housing of its wealth-storage function entirely. Because houses depreciate rather than appreciate, Japan builds continuously.

In Tokyo, more housing permits are issued annually than in the entire state of California, yet rents have remained broadly flat for decades. Without expectations of capital gains, there is far less political pressure to restrict supply.

Australia sits in the middle alongside New Zealand, Canada, the UK, and the US. These markets are the “homeownership dream” cluster, yet within that shared dream are differences worth learning from.

The US is the most instructive divergence. While Australia’s outright ownership rate has drifted downward, America’s has climbed steadily from 21.5 to 26 per cent over the same period.

Its 30-year fixed-rate mortgage locks borrowers into a rate for the life of their loan, converting debt into equity on a predictable schedule. Australia’s variable-rate mortgage culture works in reverse: every rate rise hits borrowers immediately, and low rates have historically encouraged equity extraction rather than paydown.

The United Kingdom offers a different lesson. Rather than building a strong private rental market, Britain bifurcated: you either owned your home or were housed by the state. As Right to Buy policies sold off council stock from the 1980s onward and ownership became unaffordable for a new generation, there was no adequate private rental sector to absorb the overflow. The UK’s housing crisis is, in part, the cost of never having built one.

Canada and New Zealand most closely mirror Australia: high mortgage dependence, minimal social housing, and a private rental sector that expanded not by design but by default.

The Australian Dream is not dead. But it has been quietly privatised.

Incentives like first-home buyer grants and Help-to-Buy schemes temporarily boost individual access but inflate prices, benefiting existing owners and undermining their own goals.

The single most transferable lesson from the OECD data is that countries with functioning housing systems, whether ownership-based like the US or rental-based like Germany, built them through deliberate, tenure-neutral policy sustained over time.

The idea of a quarter-acre block may have shrunk, but the dream of a home you can call your own does not have to.

Experts weigh in on investment markets

Global financial markets continue to gyrate wildly depending on the Middle East conflict and the latest utterances from President Donald Trump. It can be confusing for investors.

The last thing you want to do is panic and retreat to cash - I’ve shown enough examples in the past of why that strategy can be such a mistake.

But what do you do?

Independent investment platform InvestmentMarkets asked 10 leading fund managers, market strategists and sector specialists across equities, fixed income, property, private credit and global macro to cut through the noise.

Each offers a distinct perspective on where the risks and opportunities sit heading into the second half of 2026:

Darren Connolly, CEO, InvestmentMarkets

“Most investors think they’re diversified, but true diversification means more than holding a few different stocks. It means exposure across asset classes, geographies and income sources -and it means having parts of your portfolio where the cash flows aren’t driven by market sentiment at all. That’s the gap we see most often, and it’s the one that hurts most in periods like this.”

Michael McCarthy, CEO, Moomoo ANZ

“I’m seeing signals from bond markets, currency markets, cryptocurrency markets, and share markets that are all lining up with the same message... growth is slowing and interest rates are headed higher. The best time to prepare for volatility is at the beginning when you devise your strategy. The next best time is when markets are going well. The third best time is now, because it’s never too late to act.”

Rudi Filapek-Vandyck, Founder, FNArena

“The sharemarket outside of a very small selection of winners is now basically becoming a value proposition for investors who can look beyond the immediate headwinds. The whole AI narrative is a very long-term story. It’s going to change the world, have no doubt but the way it does is open for debate.”

Simon Raubenheimer, Director, Contrarius Investment Management

“It is tempting to get excited about shares that are down 70 to 80 per cent in a short space of time, but there’s a serious risk of buying a value trap. Our challenge is to be extremely disciplined in avoiding companies that face existential risks, even if they look cheap in the rearview mirror.”

Marc Jocum, Product and Investment Strategist, Global X

“The current dividend yield on the Australian sharemarket is around 3.2 per cent, the lowest it’s been for decades. We are heavily weighted into financials and materials, which make up 50 to 60 per cent of the market, and significantly underexposed to the sectors projected to grow earnings at double digits. Don’t forget that earnings drive the majority of share market returns.”

Michael Saba, Portfolio Manager, Arculus Funds Management

“The landscape has changed dramatically. Hybrids are being phased out, but that doesn’t mean they’re dead, there are still 38 issues and around $37 billion outstanding. What’s exciting is the range of new yield products emerging. It’s a sector that has just reached adolescence - it’s going through growing pains, and that’s good, because it will sort itself out.”

Nick Alcock, Australian Secure Capital Fund (ASCF)

“Since October 2021, APRA has maintained a 3 per cent mortgage serviceability buffer. The unintended consequence is that we now see situations where hopeful refinancers can’t even service with their current lenders. Borrowers still need funding and projects still need finance, but the traditional banking system is no longer willing to provide it in some cases and that’s the gap private lenders have stepped in to fill.”

Vaughan Hayne, Managing Director and Co-Founder, Exceed Capital

“We’ve seen rents on the Gold Coast increase 40 per cent in two years, with A-grade office vacancy under 1.7 per cent, the lowest it’s ever been. Some of our A-grade buildings have moved from $460 to $650 per square metre. Construction costs and labour costs are at record highs, which means less new supply ... which is generally a good thing for existing commercial property owners. Less supply, more demand, pushes up rental prices.”

Michael Fazzini, Sales and Distribution Executive, Capru

“The biggest insight in property development that most investors don’t realise is that most of the profit comes from what you pay for the land. Market price for land in our world isn’t the last transaction of a similar site or per square metre, it’s working backwards from what the finished product is worth, the build costs, and the minimum return needed to make the project viable. Get that wrong and no amount of execution can save you.”

Marcus Cleary, Head of Distribution, Oreana

“Volatility is a pricing problem, not a cash flow problem. Whether it’s tariffs, tech selloffs or oil shocks, the price volatility and breadth of that volatility isn’t seen within the direct asset class because the cash flows we deliver are linked to CPI and backed by long-term leases. Regardless of the economic environment, families are still sending their kids to childcare.”

Richard Collier, CFO, Heartland Bank

“Australians aged over 60 hold more than $3 trillion in property, yet less than 1 per cent of that available equity has been unlocked. The total reverse mortgage market is only around $5.5 billion against an addressable market of around $600 billion. With superannuation balances of just over $4 trillion across the entire system not sufficient to fund the lifestyle Australians expect in retirement, this is the largest store of value that remains untapped.”

Signs the property market is becoming fragile

As I always say, investment markets are primarily driven by the psychology of participants -and when it comes to property, boom-time psychology is shifting depending on the asset class.

Australia’s property market has entered a confidence slowdown, with the Australian Property Institute’s Property Market Outlook Index falling to 6.1 in this current quarter - down from 7.1 in the March quarter and 7.3 in the December quarter of last year.

The decline spans all five major states and every key asset class - the sharpest signal yet that the Reserve Bank of Australia’s February and March cash rate increases have reset expectations across the market.

The survey of 247 property professionals, found the interest rate outlook has now become the single biggest source of downward pressure on property prices across the key asset classes. Even so, the national index remains above the neutral level of 5 points, suggesting the market is slowing sharply in sentiment terms rather than tipping into outright weakness.

Industrial property has emerged as the market’s strongest-performing asset class. Office and retail have now recorded sub-neutral sentiment in two consecutive quarters, with both sectors sitting below 5 points.

Industrial property is now the standout performer, residential remains supported by structural undersupply, and office and retail continue to struggle below neutral as higher rates and weaker business and consumer confidence bite.

Industrial property has overtaken residential as Australia’s most resilient property asset class, scoring 6.8.

E-commerce demand for warehouses, continued infrastructure investment, technological development and mining activity are all keeping the sector strong while confidence softens elsewhere.

The gap between industrial and office tells the story of the quarter. Industrial scores 6.8 against office’s 4.6, a difference of 2.2 points. Every state’s industrial score sits above the neutral threshold, with Western Australia strongest at 7.5, South Australia at 7.3 and Queensland at 7.2.

Residential property recorded the sharpest single-quarter fall of any asset class, dropping from 7.2 in the March quarter to 6.2 in this quarter. It remains the second-strongest sector overall and well above the neutral level.

That’s because the housing supply crisis has not gone away. The ongoing lack of new and existing housing supply, continued population growth, and the Federal government’s 5% Deposit Scheme are still exerting upward pressure on residential prices even as confidence falls.

Office sentiment edged down from 4.9 to 4.6 between the last two quarters, with Victoria the weakest market nationally at 3.6.

Office valuers cite the interest rate outlook, weakening business confidence, and the evolving nature of work as the main sources of downward pressure, including AI adoption and ongoing work-from-home arrangements.

New South Wales is the weakest state for the office market, while South Australia, WA and Queensland are stronger.

Six months on, the 5% Deposit Scheme ignites the lower end of the property market

New analysis from property research giant Cotality shows that since October last year, properties with an estimated value below the 5% Deposit Scheme price caps have recorded stronger growth than higher-priced homes.

Over the first six months of the expanded scheme, homes with a value under the price caps have increased in value by 6.7 per cent compared with a 3.6 per cent rise in value for properties with an estimated value above the price caps.

Source: Cotality

According to Cotality, several factors may explain the stronger growth at lower price points:

Demand brought forward: Anticipation of increased competition and price pressure after the scheme’s launch has likely brought forward demand from those who didn’t necessarily need to rely on the deposit guarantee.

Serviceability constraints: With higher home values and elevated interest rates, serviceability constraints are likely to be pushing demand toward lower-priced, more affordable properties.

Investor activity: Investor activity has increased in the lower price segment, competing with first-home buyers and mainstream demand. Investors accounted for 40 per cent of mortgage demand at the end of last year - well above the decade average, where they typically make up around one-third of mortgage demand.

Sydney had the largest value growth differential where homes with a value under the cap are up 4.1 per cent over the past six months, while those above the cap have fallen by 1.1 per cent.

Across Australia, 81 of the 88 city and regional markets have shown a stronger growth rate for properties with a value under the price caps.

Overall, it is likely the first home buyer deposit guarantee will gradually lose its stimulatory power, with more homes exceeding the price thresholds and a growing share of prospective buyers running into a finance hurdle that is set to rise further.

Demand from first time buyers looking to purchase a house is likely to be skewed towards the outer fringes of the capital cities or regional markets where price points are lower.

More affordable and widespread options are available to first home buyers across the unit market, which is likely to become an increasingly popular option for budget conscious buyers looking to participate in the deposit guarantee scheme.

Smart ways to save $50 a week on fuel

Right now, there’s a bit of breathing room at the petrol pump, helped along by the temporary halving of the fuel excise, but it may not last long. Fuel price cycles can turn quickly, and it doesn’t take much in an oil crisis for costs to spike again, leaving drivers wincing at the bowser.

Last month, prices surged above $2 a litre in most capitals, climbing into the mid-$2 range on the worst days of the cycle before easing again.

Diesel, which fuels freight, tradies and supply chains, prices remain above $3 a litre in some parts of Australia due to ongoing instability in the Middle East.

And as I’ve been saying for a while, fuel prices don’t just stay at the pump. They ripple through everyday life, from higher grocery bills and rising call-out fees to even small daily purchases gradually costing more than they did not long ago.

While we can’t control global oil markets or volatile price cycles, we can be more mindful about how and when we use our car when prices soar and hit our household budgets.

Here are some practical ways to ease the financial squeeze:

Multiple car trips → One planned shop

Ditch the “quick dash” for one or two items and commit to a weekly shop. Be disciplined... If dinner is missing an ingredient, work around it. That single tomato for taco night can end up costing far more in fuel to get it from the farm to the supermarket, and then home to you.

The same goes for planning your week and consolidating car trips where possible. If you’re already dropping your kid at soccer training, pick up bread and milk on the way home instead of making a separate trip in the morning.

Home delivery → Click and collect

Delivery fees have been creeping up. Click and collect offers a similar but cheaper alternative... your order is packed and ready, without paying for home delivery.

Pair pick up with an existing trip to avoid an extra journey.

Short drives → Walking or cycling

Short trips are the least fuel-efficient. A cold engine can use two to three times more fuel per kilometre before it warms up, making quick 1–2 km drives disproportionately expensive.

All those short errands across a week can quietly add up. So if it’s walking or riding distance, consider skipping the car... your wallet and health will thank you.

Filling up anytime → Timing the fuel cycle

Fuel prices move in cycles, and timing matters. Filling up just before the weekly spike can save several cents per litre, and a few dollars per tank.

Using a fuel price tracking app like Simples, FuelCheck, PetrolSpy or MotorMouth can help you spot the cheapest days and stations near you.

Peak-location refuelling → Slight detours

High-traffic service stations, especially in CBDs and along highways, are often more expensive.

A short detour off-route to find a cheaper retailer can deliver decent savings over a full tank. Differences of 20-60 cents per litre are not uncommon during peak cycles.

Multiple tradies → One handyman visit

Most tradies drive diesel-guzzling utes, and the extra they are paying in driving to your house is passed onto you in the form of higher call-out fees.

Instead of booking multiple tradies for various small jobs, bundle tasks together and arrange for a single handyman visit who can handle them all. This will not only cut down on bills but also added fuel costs factored into them.

Last-minute takeaway runs → Planned meals

How often do you jump in the car for dinner because nothing’s planned?

When fuel is expensive, that quick takeaway can cost far more once petrol and higher food prices are factored in. Keeping a simple backup meal in the fridge, like a pre-cooked lasagne, is an easy way to avoid the extra trip and expense.

Big car → Small car/EV

If you have a smaller car in the family, make it the ‘default’ runabout choice. If you have an EV, well, that's a no-brainer preference.

Ask everyone to start using the most fuel-efficient car, even if it’s a borrow, to save on family fuel expenses.

Driving to work daily → Mix it up

If possible, swap in public transport, carpooling, or even a work-from-home day or two. Cutting just a couple of commutes a week can save significantly.

Air conditioning → Fresh air

Car air conditioning increases fuel use, particularly at lower speeds.

When it isn’t a heatwave, try opening the windows instead of relying on the AC and enjoy the fresh air.

Neglected car → Well-maintained vehicle

Poor maintenance reduces vehicle efficiency. And dirty air filters, old oil and misaligned wheels all increase fuel use, as well as wear and tear.

Regular car servicing may feel like an expense, but it often prevents larger costs later.

It all adds up

Making a few of these small changes across the week can easily add up to $50 or more in savings ... or more than $2,500 a year.

That’s money that would otherwise disappear into the tank.