- Your Money & Your Life

- Posts

- Oil crisis: The scary truth + The crushing of Australian households

Oil crisis: The scary truth + The crushing of Australian households

My Money Digest - 27 March 2026

David Koch

March 27, 2026

Hi everyone,

Late last year my brother bought an electric vehicle. Like so many EV owners, they have to be pretty smug as the rest of us worry about rising petrol prices.

As I’ve written about before, if you are buying an EV be careful of car insurance premiums. They have been rising fast and there are big premium differences between insurers ... so shop around.

In this newsletter:

The crushing of Australian households.

Inflation rate slows ... but it’s before the Middle East crisis.

Higher oil prices push up more than petrol prices.

Diesel prices hit farmers.

The gold boom busts. What to do?

Interest rate rise spooks property buyers.

Which countries buy the most Chinese EVs?

The crushing of Australian households

After last week’s Reserve Bank interest rate increase, I warned of the possibility that rising rates coupled with rising petrol prices had the possibility of crushing Australian household budgets.

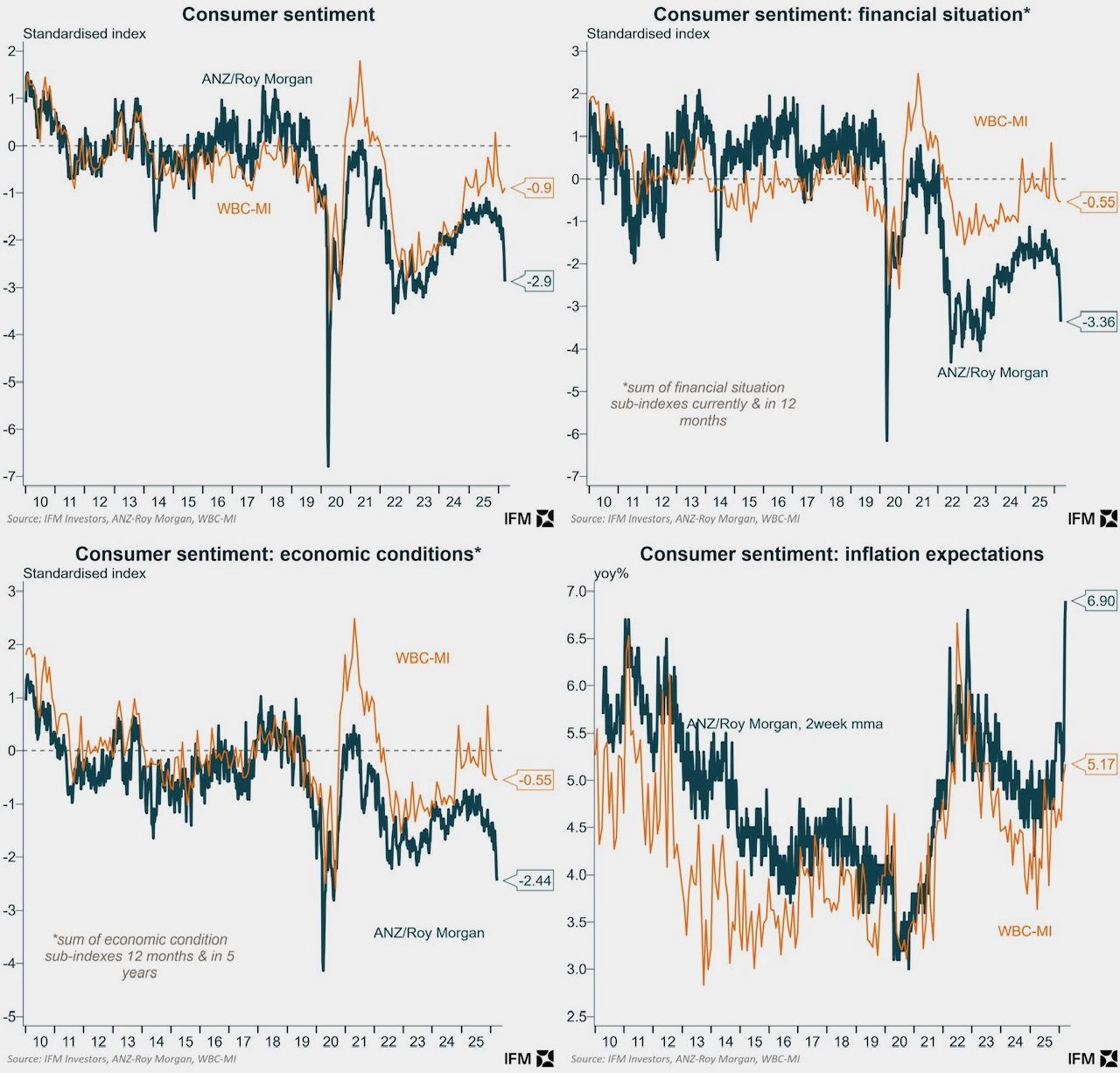

Reinforcing my point, this week’s ANZ-Roy Morgan consumer confidence figures are down 20 per cent - the worst result since the oil crisis in 1973.

Consumers expect inflation to soar to 6.9 per cent, while the number of people who believe it is a good time to buy a large household item is in freefall.

The RBA’s 0.25 percentage rate rise this week, taking the cash rate to 4.1 per cent, has added about $94 a month to repayments on a $600,000 home loan. It was the second consecutive increase, following the February board meeting hike, and a third straight rise is expected at the next RBA board meeting in May.

Add the two consecutive rate rises together and average the repayments on the average home loan ($694,000-$736,000) will be up around $200 a month … After a third hike, it would be almost $300 a month.

Then add the extra $100 a month ($25 a week on a 60 litre tank) to fill a car since the Middle East crisis started lifting global oil prices, and Australian household budgets are being hit hard. The lift in petrol prices is about the same as a 0.25 per cent rise in interest rates.

If household sentiment and spending crashes... economies tend to follow.

Be careful.

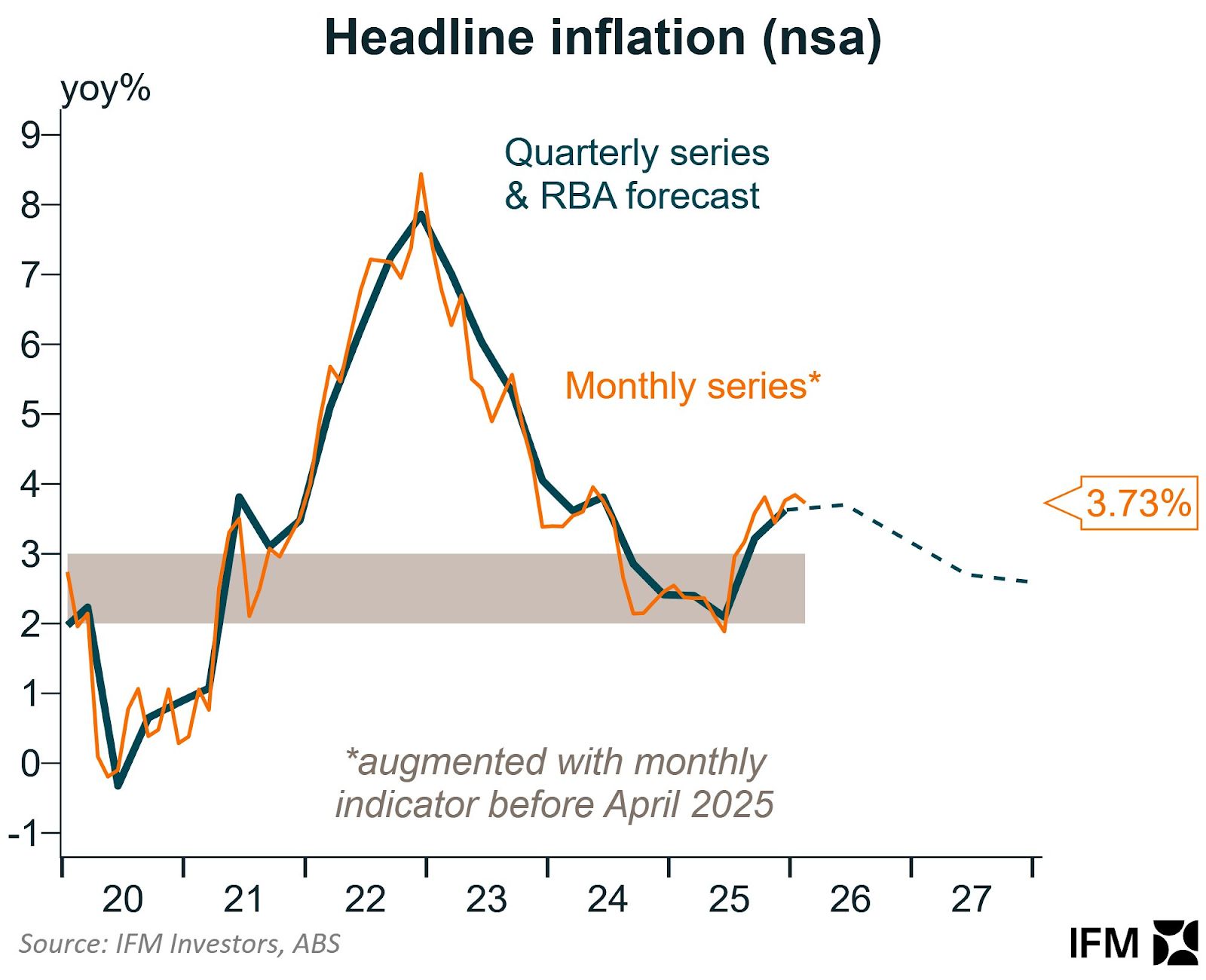

Inflation rate slows, but that’s before the Iran conflict …

I often warn people to be wary of economic figures that look in the rear vision mirror rather than reflect reality. Wednesday’s inflation result is a classic example.

Headline inflation slowed from 3.8 per cent to 3.7 per cent - still above the RBA’s preferred 2-3 per cent target range, but trending back to it.

By contrast, the confidence figure was measured last week, while the CPI figure reflects data from February - before the Middle East crisis began. It’s hard to believe the first attack on Iran was on 1 March - it seems to have been going so much longer!

This time next month when the March CPI is released, we will be given a much better indication of the impact of rising oil prices (and crumbling consumer confidence) on inflation.

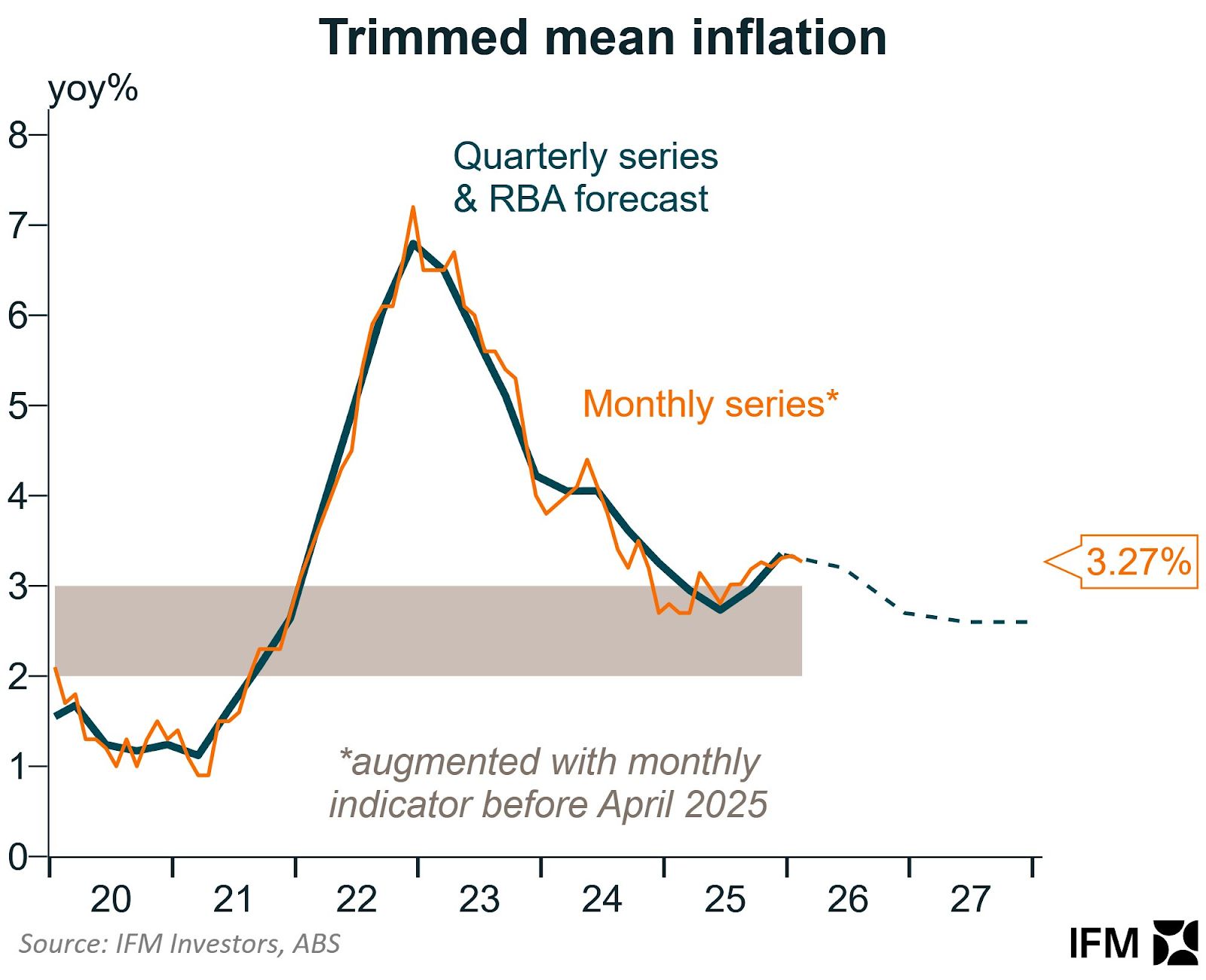

The trimmed or core inflation annual figure, closely watched by the RBA, was steady at 3.3 per cent.

Treasury modelling shows inflation could hit 5 per cent this year and that growth may be constrained for the rest of the decade, but Treasurer Jim Chalmers believes that may be too conservative.

The key drivers of inflation in February were housing, which rose by 7.2 per cent; food and non-alcoholic beverages, up 3.1 per cent; and electricity, now up 37 per cent over the year.

The Australian Bureau of Statistics said the sharp annual jump in electricity costs was largely due to the roll-off of both state and Commonwealth electricity rebates, though it noted prices still rose by almost 5 per cent even excluding the impact of those rebates.

Higher oil prices push up more than just the cost of petrol

The economic fallout of a closed Strait of Hormuz extends far beyond what it costs to fill up your car. The Gulf is not just a petrol pump. It is the gate for fertiliser, petrochemicals, aluminium, helium, and refined fuels.

Every day the strait remains shut, a chain of industrial dominoes topples across continents.

Asian refineries - where we buy our petrol - are built to process the Gulf’s heavy, high-sulphur crude and are now struggling to adapt to lighter alternatives being sourced elsewhere.

This is affecting the supply of diesel and jet fuel — the two products in shortest supply. Processing cuts of 5 to 15 per cent have hit refiners in China, India, Japan and Thailand, with China suspending all refined product exports entirely.

Then there’s the chemistry problem. The Gulf accounts for 45 per cent of global seaborne naphtha flows and 23–30 per cent of exports of key plastic inputs, including styrene and polyethylene. As a result, several Asian manufacturers have halted production.

The active compounds in most pharmaceuticals, from aspirin to antibiotics, require petrochemical feedstocks that China and India source heavily from the region.

Qatar’s Ras Laffan complex, shut since an Iranian drone strike, also produced roughly a third of the world’s helium - a gas essential for cooling the super magnets in semiconductor fabrication that power the world’s data centres. There are no ready substitutes.

And then there’s the impact on food. The United Nations estimates that a third of global seaborne fertiliser trade passes through the Strait of Hormuz. Since the war began, urea prices have risen 35 per cent and sulphur is up 40 per cent. With spring planting imminent across the northern hemisphere, farmers face a horrible financial conundrum: pay vastly more for inputs, reduce application rates, or plant less maize and wheat.

The poorest countries are absorbing the worst of it. In Nepal, cooking gas is being rationed. In Sri Lanka, firms have been told to shut on Wednesdays. In Pakistan, schools have closed and universities have moved online.

Even if the war ended this week, experts say it would take months for energy markets to regain some semblance of normality. Production restarts take weeks, Qatar’s damaged liquefaction units require three to five years of repairs, and the global tanker fleet is in the wrong ocean. War-risk insurance has been cancelled across the Gulf, and insurers are unlikely to reprice quickly. Fertiliser that arrives weeks late cannot be used for the 2026 harvest.

As a net energy exporter, the United States is insulated from the worst excesses of an oil crisis, compared to many allies and trading partners in Europe and Asia.

Diesel prices hit our farmers

The international benchmark price for refined diesel has more than doubled, up 109 per cent according to the ACCC.

And regional Australia is carrying the full weight of that.

According to Ray White’s head of research, Vanessa Ryder, for a grain farmer running a 900-hectare operation through seeding, or a beef producer moving cattle across multiple properties, the cost of diesel is not just a line item - it is the difference between a viable season and one that isn’t.

Unlike petrol, diesel has no retail price cycle. It moves directly and immediately with international benchmarks, and with around 90 per cent of Australia's supply imported, there is no domestic buffer.

Fuel wholesalers have suspended spot-market sales, prioritising contracted customers and leaving smaller, regional operators to manage the limited supply they have on hand.

The wholesale picture underscores the structural nature of the problem. The national average diesel wholesale price over the past twelve months was 168.5 cents per litre; it is now 300 cents. That is not a spike that just gets absorbed quietly at the farm gate.

Reports of diesel theft from farm machinery and storage tanks have risen sharply across Victoria, NSW and Western Australia, a sign of how acute conditions have become on the ground.

Farmers can access the fuel tax credit scheme to offset some excise costs, but that mechanism provides no relief against the underlying international price movement.

The downstream effects will take time to fully show, but the direction is clear. Higher operating costs for broadacre cropping, livestock transport, and freight feed through to food prices.

The farm diesel crisis is not a story that stays on the land. It ends up in the weekly grocery bill.

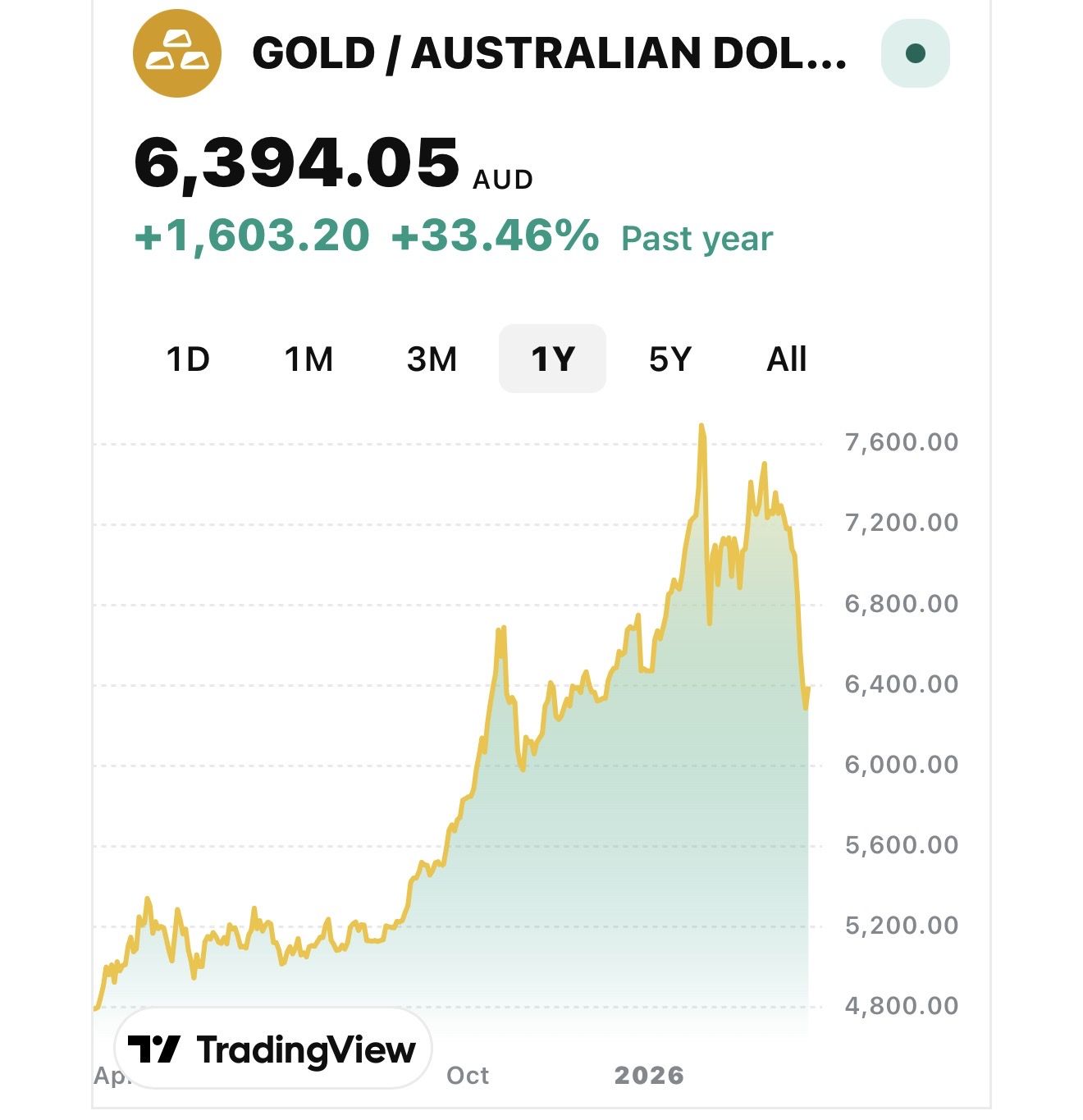

The gold boom busts

A couple of weeks ago I was asked my opinion in TV interviews about the queues of investors lining up and down the street outside gold bullion stores. I explained that, for me, it was a sign that gold was at its peak and investors should be cautious. It was a classic case of an investment bubble about to burst.

Since then, precious metals investors have been rattled. Gold is down 22 per cent from its peak earlier this year, while silver has tumbled 50 per cent from its high. Bond yields have spiked on inflation fears, and the market is treating it as a breakdown.

New gold investors have been shocked and many have cut their losses and run.

But Mark Moreland from MPC Markets thinks that rather than running, investors should be looking to either hang in there or average down.

Most analysts are reaching for the 1970s stagflation playbook, but Mark thinks that’s the wrong map.

He says a far more precise analogue is the 1990 Kuwait invasion, when an oil-driven inflation shock pushed yields higher and precious metals lower. After a swift military resolution collapsed oil prices, growth fears took over, and yields fell by roughly 80 basis points by the ceasefire, with metals climbing back alongside rates.

According to Mark, that is the pattern playing out right now. And it creates a three-phase entry opportunity that disciplined investors should not be sleeping on.

The structural case remains completely intact. De-dollarisation is accelerating. The US debt spiral is worsening. The recession outlook sits at 50/50 with inflation - that refuses to fully retreat.

These forces do not disappear when a conflict de-escalates. If anything, they become the dominant narrative in Phase Three - and that is precisely when gold and silver's secular uptrend resumes with force.

Mark says this sell-off is technical. It is positioning-driven. It is not a fundamental breakdown.

Interest rate rise spooks property buyers

The first weekend after this latest interest rate rise from the RBA saw combined capital city auction clearance rates come in at 62.7per cent. It’s the weakest so far this year, and on par with the low point recorded at the end of the auction season in mid-December last year.

Every capital city recorded a decline in the preliminary clearance rate relative to the week prior.

The soft auction result comes as the volume of auctions ramps up, with 2,857 homes taken under the hammer last week, 2.4 per cent more than the previous week and the second highest weekly number of homes taken to auction so far this year.

The volume of auctions is expected to rise further this week, with more than 4,000 homes currently scheduled for auction in the week leading up to the Easter long weekend. This period typically marks the seasonal high point in auction activity.

Melbourne: Second-highest volume so far this year - 6.2 per cent higher than last week and 15.6 per cent above the same time last year. The clearance rate was 64.2 per cent, down 2.7 per cent from the previous week and the weakest since April 20 last year.

Sydney: Auction volume rose 2.4 per cent from the previous week and is 24.4 per cent higher than the same week last year. Clearance rate was 60.8 per cent, the lowest early result since mid-December last year.

Brisbane: Second-highest volume this year, 37.9 per cent more auctions than the same time last year. Clearance rate 65.3 per cent - the lowest since the week ending 21 December.

Adelaide: Volumes fell 14 per cent for the week but were 8.3 per cent higher than the same time last year. Clearance rate dropped sharply to 65.4 per cent, the lowest since the first week of August last year.

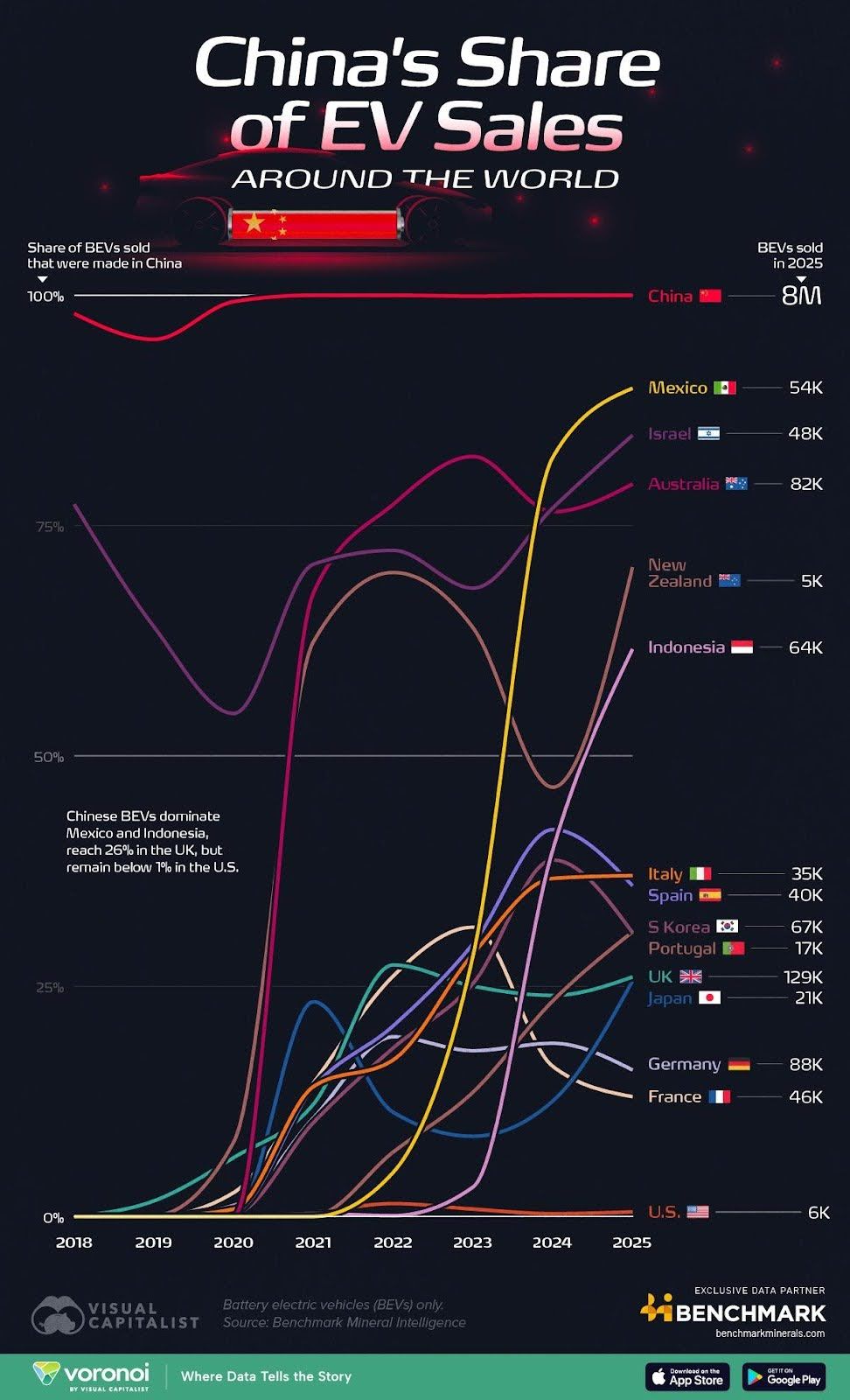

Where the most Chinese electric vehicles are sold

Have a great week, everyone.