- Your Money & Your Life

- Posts

- My rate cut call + The Chinese AI corp spooking the BIG 7

My rate cut call + The Chinese AI corp spooking the BIG 7

My Money Digest - 31 January 2025

David Koch

January 31, 2025

Hi everyone,

When I was going to the gym on Wednesday, a parking attendant stopped me. He wanted to tell me that he had been with the same car insurer for 20 years and had automatic annual renewal with them. And every year his premium went up and he had never made a claim. His wife was so annoyed that she decided to compare the market to see whether she could find a better deal.

She did. Same cover but with a premium of $1,200 less than what she was paying. They have another car and a boat that they still have to compare.

Libby’s mantra “never automatically renew an insurance policy” rings true again.

In this week’s newsletter:

December quarter CPI is good news … and a rate cut is on the way!

‘The Magnificent Seven’ get a wake-up call.

CoreLogic’s residential property forecast for 2025.

7 property myths BUSTED.

Beware of these dodgy tax schemes.

The 15-minute money challenge all couples should do.

A late Christmas present for Federal Treasurer Jim Chalmers

The upcoming Federal Election (likely to be held in April) will be fought on one major issue … cost of living.

That’s why Wednesday’s December quarter CPI figures were so crucial. A good result would encourage the Reserve Bank to cut interest rates at its February board meeting. A bad result would likely delay the next rate cut until after the election.

Jim Chalmers must have been on tenterhooks Wednesday morning... and breathing a sigh of relief when the better-than-expected CPI figures came through.

Financial markets are now factoring in an 80 per cent chance of a 0.25 per cent interest rate cut at the RBA’s mid-February meeting. That will be a welcome relief for mortgage holders and mean extra cash will help ease the cost of living pressures.

Headline CPI rose by 0.2 per cent for the December quarter, which was lower than the 0.3 per cent expected by most economists. The annual rate dropped to 2.4 per cent from 2.8 per cent in the previous quarter.

But, of course, The RBA constantly tells us that it ignores the headline rate and focusses on the ‘trimmed mean’ which takes out all the volatile elements of the CPI basket of costs. In the December quarter the RBA’s preferred underlying inflation measure, the trimmed mean CPI, rose by 0.5 per cent which was, again, below the 0.6 per cent forecast by economists.

Back in November, in its Statement of Monetary Policy, the RBA thought the December trimmed mean would be 0.7 per cent. The 0.5 per cent this week is well under its prediction. That’s good news.

As I said, if you annualise the last six months of trimmed mean CPI results, it would show 2.7 per cent (and within the RBA target range for a rate cut) rather than the current annual of 3.2 per cent.

Now before you accuse me of fiddling the figures to make the CPI figure look better than reality, hear me out.

Economies can move quickly and economic data can sometimes be slow to show more recent and relevant trends. It’s the end of January and the current CPI annual figure counts everything that was happening at this time last year.

That’s a long time ago.

What economists, and the Reserve Bank, are looking for are trends. How quickly the economy is moving both up and down. Monetary policy has to be quick on its feet.

Keeping rates too high for too long means the economy could slow more than you want and it is slow to turn around.

That’s why, in this instance, the six month figures are important. It shows inflation is getting back under control over recent times. Consumers are in the bunker even though governments are spending up big and not helping the economic figures.

The Magnificent Seven get a wake-up call

America’s seven big technology behemoths had a wake-up call during the week when China showed they can mix it with the best when it comes to artificial intelligence (AI).

Microsoft, Apple, Alphabet (Google), Meta (Facebook/Instagram) Tesla, Nvidia and Amazon fuelled global sharemarkets in 2024 based on how they will be able to leverage AI. Investment markets basically believed they would control the world of AI.

But it seems their moat surrounding AI development may not be as wide and deep as they expected with China’s DeepSeek releasing a powerful and cheaper version of AI.

It sparked financial ructions around the world and triggered a big selloff in technology shares, particularly AI chip maker Nvidia.

If anything, it shows just how wild technology stock investing can be and that you need the right risk profile, as an investor, to be able to cope with it..

CoreLogic’s property forecast for 2025

It’s the start of the year and it’s when the investment gurus unveil their thoughts for the year ahead. CoreLogic is arguably Australia’s premier property research group and its Head of Residential Research, Eliza Owen, has polished her crystal ball. She is predicting:

Lower interest rates will boost housing values and transactions, but not by much

Interest rates might be cut in early 2025 as inflation continues to drop, with annual core inflation falling to 3.2 per cent in November (below the RBA forecast of 3.4 per cent for December). Two of the big four banks are currently expecting a rate cut in February.

The industry should brace for the possibility that rate reductions may have little effect on home values and transaction activity this year. Even if the average mortgage rate drops by 1.35 per cent (the lower-bound of forecasts for the cash rate at the end of 2025), a median-income household could reasonably afford a $593,000 home - still much lower than the current median home value of $815,000.

A rate of 3.1 per cent by the end of 2025 is also higher than the pre-COVID, decade average (2.55 per cent) that supported strong lending volumes in the 2010s.

A potential window into how Australians would respond to higher borrowing capacity is the stage 3 tax cuts from 2024. While this would have boosted borrowing capacity through higher net income, the housing market saw an anaemic response, with growth in values slowing from June 2024.

Lending policy could amplify, or nullify, the impact of rate reductions

Changes to macroprudential settings (the policies used by regulators to reduce credit risk and support financial stability), will likely affect the availability of housing finance.

Lowering the mortgage serviceability buffer from 3.0 percentage points to 2.5 percentage points (a reversal of the increase in October 2021) could boost home buying activity through increased borrowing capacity. However, this action from the regulator isn't guaranteed.

According to APRA's November statement, the risk of financial shocks hasn’t abated, and regulators have warned that high household debt levels are a major concern. If household debt levels rise as interest rates fall, APRA could introduce new measures, such as limits on high loan-to-value ratio (LVR) or high debt-to-income (DTI) lending, such as what New Zealand’s central bank (RBNZ) has implemented there.

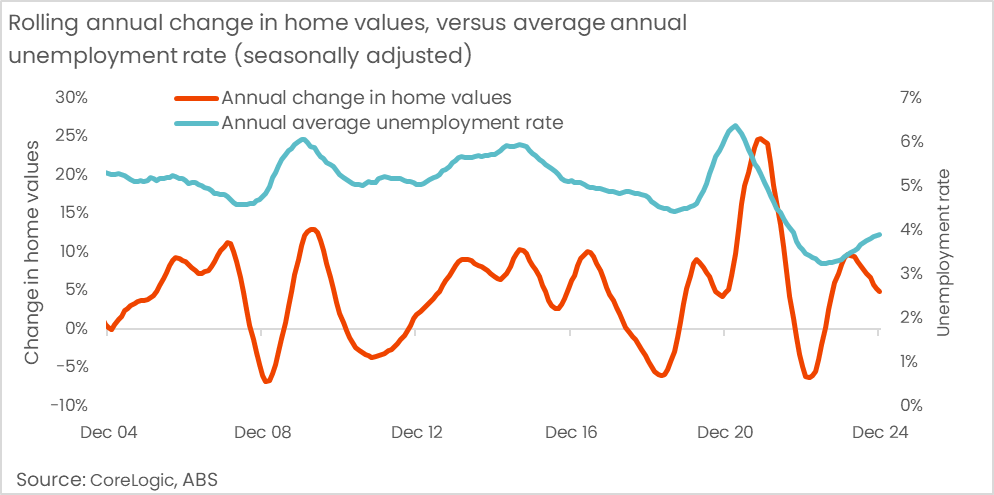

Unemployment to rise, but unlikely to negatively impact housing values

The RBA forecast unemployment to rise to 4.5 per cent by the end of 2025, but so far the labour market remains tight, and the unemployment rate is at just 4 per cent (the pre-COVID, decade average was 5.5 per cent).

Assuming that the labour market does loosen this year (which is an expected result of lower inflation and economic demand), we might not expect much of an impact on the housing market. For the past two decades, there has been a mildly positive relationship between the unemployment rate and housing values, potentially because periods of rising unemployment trigger lower interest rate settings to stimulate the economy.

For those who remain employed in 2025, lower inflation will also provide a boost to real incomes that could be put towards a deposit or housing transaction costs.

The devil will be in the detail of a looser labour market and its impact on housing in 2025.

For example, rising periods of unemployment have historically impacted younger Australians (i.e. 15–24yr olds) more than other age groups, and these younger Australians are more likely to be concentrated in the rental market than in home ownership, thus having more of an impact on rental demand. However, there may be localised impacts on housing demand and value depending on industries and regions that face greater job losses.

Net overseas migration will continue to slow, taking some demand pressure off the rental market

Net overseas migration peaked at 556,000 in the year to September 2023 and fell to 446,000 by June 2024. According to the Centre for Population, it is expected net migration will continue declining to about 340,000 by mid-2025 as the 'COVID-catch up' effect fades as more short-term migrants leave.

While overseas migration isn't the only factor flowing through to rental demand, significant changes in migration patterns have impacted the market. The chart below compares the historic exposure of individual ‘SA4 markets’ (Australian regions that represent labor markets) to net overseas migration with rental value changes between September 2023 and December 2024.

Areas with high migration saw a substantial increase in rents in 2022 when border restrictions eased. Now, the slowdown in overseas migration appears to be reducing demand more quickly in these same rental markets.

Residential construction will remain low, but cost pressures could stabilise

New home approvals are low, with only 169,000 new dwellings approved by November 2024. This is a 24 per cent drop from the decade-average and is 30 per cent below the Housing Accord's average annual target (240,000).

High construction costs, land costs, and interest rates, along with potentially diminished buyer confidence in the new home sector, have dampened approval numbers. There are some signs of a pickup, with dwelling approvals bottoming out in early 2024, which is most obvious in high capital growth markets like WA, SA and QLD.

Interestingly, about 250,000 approved dwellings are still incomplete. The slowdown in building activity will eventually ease capacity constraints, allowing for more timely delivery of homes and clearing the backlog. However, competition from public infrastructure sector for labour and input materials is likely to remain substantial. Continued government support and business investment are essential to boost productivity in residential construction.

Overall, despite rate cuts and easing inflation, 2025 is expected to see lower value growth and sales numbers than last year. This could involve a shallow downturn in values at the start of the year, followed by a mild recovery as inflation and interest rates move lower, real incomes rise and housing supply remains low.

7 property myths BUSTED

Property markets constantly generate debate and discussion, often leading to misconceptions about how they work. These myths can influence decisions about buying, selling, or investing in property - sometimes leading people to miss opportunities or make choices based on incorrect assumptions.

Ray White chief economist, Nerida Conisbee, examines some common property market myths and uncovers the reality behind them.

There is an ideal time to buy a house

Market timing in property is risky, as we've seen experts with extensive data get predictions wrong. When you add high transaction costs like stamp duty, legal fees, and moving expenses, trying to time purchases can be costly.

The best time to buy, sell, or invest in property is simply when you're ready - with enough savings, stable income, and clear housing needs. Making property decisions based on your situation rather than market predictions usually works out better.

House prices double every 10 years

While it's commonly claimed that house prices double every 10 years, the reality is more complex and heavily dependent on location and timing. Different cities and regions can experience vastly different growth rates, with some areas seeing prices more than double while others might see modest growth or even decline. Local economic conditions, infrastructure development, and population trends all play crucial roles in determining property price movements.

Property price growth tends to move in cycles rather than following a steady upward trajectory. Markets typically experience periods of strong growth followed by stabilisation or occasional declines. Rather than relying on a "doubling every decade" rule of thumb, buyers should focus on their own circumstances and ability to hold property long-term to weather these market fluctuations.

House prices could see a sharp correction so I should wait to buy

Housing markets have proven remarkably stable, even during major economic shocks. The 2007-09 financial crisis and COVID-19 pandemic only saw brief price drops of around six per cent before recovering. In Australia, strong population growth and limited new housing supply, especially in cities, continue to support prices.

While housing affordability is a real concern, several factors prevent major price drops: strict building regulations limit new housing, population growth drives ongoing demand, and job concentration in cities keeps urban housing in high demand. Instead of a sharp correction, history suggests we're more likely to see periods where prices level out before growing again.

Rents are rising because of landlords

Rental prices are primarily driven by market supply and demand, not individual landlord decisions. When there are plenty of rental options available, tenants can simply choose cheaper properties, forcing landlords to keep rents competitive or risk having empty properties and no income. Landlords generally can't raise rents above market rates because tenants will move to more affordable options.

What actually drives rent increases is the balance of rental properties versus people looking to rent. When there's strong demand (due to factors like population growth, more international students, or people unable to buy) but limited rental supply, competition among tenants pushes rents up. Recent rent rises have more to do with housing shortages and increased demand than individual landlord decisions. This is why we often see rents stay flat or even fall in areas with lots of new apartments or declining populations.

Negative gearing is to blame for Australia’s high house prices

While negative gearing makes property investment more attractive by offering tax benefits, it's too simplistic to blame it alone for high house prices. Many countries without negative gearing also face significant housing affordability challenges. The main drivers of Australian house prices include limited housing supply in desirable areas, strong population growth, strict planning regulations, and the concentration of jobs in major cities.

Property investment decisions involve many factors beyond tax benefits. Location, expected capital growth, rental yield, interest rates, and maintenance costs all play important roles.

Negative gearing is just one piece of a complex puzzle that includes broader economic factors like household income levels, lending policies, and construction costs. Looking at housing affordability through the single lens of negative gearing misses these other crucial market forces.

You are better renting and investing in shares/bitcoin/gold than buying a home

When you buy a home to live in rather than for investment, leverage is particularly powerful because you're getting two benefits: A place to live and an investment. With $100,000 saved, you could buy a $500,000 home with an 80 per cent loan. If the property goes up 10 per cent to $550,000, you've made $50,000 on your $100,000 - a 50 per cent return. Meanwhile, you've had a place to live with fixed mortgage payments instead of rising rents.

In contrast, if you rent and invest your $100,000 in shares or bitcoin, most people wouldn't borrow an extra $400,000 for these investments due to higher interest rates and market volatility. This means that same 10 per cent rise would only give you $10,000 on your $100,000 - and you'd still be paying rent. The ability to safely use leverage while getting both housing and investment benefits makes buying a home to live in uniquely attractive.

You can only afford a first home if you have money from the Bank of Mum and Dad

While parental support through the Bank of Mum and Dad helps some buyers enter the market sooner, it's not the only path to home ownership. There are multiple ways to get into the market with a smaller deposit, including government incentives like low deposit schemes without mortgage insurance, stamp duty exemptions, and cash grants for new homes. The key is understanding what you're eligible for and exploring all available options.

First home buyers can also consider alternative strategies like ‘rentvesting’ (buying an investment property while renting where you want to live), buying with friends or family members, or starting with a smaller property or less desirable location. While these options might mean compromising on your ideal first home, they provide a stepping stone into the market - remember, most people only stay in their first home for less than seven years before upgrading.

The important thing is getting into the market when you're financially ready, rather than waiting for perfect conditions or relying solely on parental support

Beware of dodgy tax schemes

The ATO is warning us to be alert for potentially dodgy tax schemes which are spreading online, including through social media.

Acting Deputy Commissioner, Sarah Taylor, is urging individuals to be wary of online promotion of tax schemes promising to significantly reduce or avoid tax altogether.

Sometimes tax schemes can be peddled as investment schemes. The ATO doesn’t want to see honest people lured into unlawful tax schemes with false promises of high returns and tax savings. If an offer seems too good to be true, it probably is.

Promoters of these schemes are often opportunistic and target vulnerable people. Protect yourself and your money by getting advice from a registered tax practitioner before committing to anything.

The ATO’s website lists a number of tax schemes to look out for. In one particular recent scheme, individuals are being advised to invest in a start-up company that allegedly qualifies as an early-stage innovation company (ESIC). By investing in an ESIC, they’re told they can then claim the early-stage investor tax offset on shares purchased through the financing arrangement.

The ATO is concerned individuals may be entering into these arrangements under the belief they are entitled to the tax benefits claimed using the financing arrangements. The ATO is also concerned that the companies may not qualify as ESICs.

Another type of tax scheme being promoted promises individuals they can avoid paying tax by setting up a purported non-profit foundation and diverting their income to it. These schemes are not effective and the individuals will still have to pay the tax on the income.

If you are approached with tax arrangements that sound like either of these examples, or sound too good to be true, seek advice from a registered tax practitioner and report it to the ATO.

The 15-minute money challenge all couples should do

Here’s a challenge: I want you to spend 15 minutes a month thinking about your money.

It doesn’t sound like much but how many people, individually or as a couple, actually sit down and think or talk about their finances? I’m not talking about paying bills, checking the credit card statement or doing the banking. That’s managing your money and very different to being informed and thinking about your financial big picture.

So often relationships are put under strain because partners don’t talk about what they each want from their money or understand where it goes. It’s crazy because financial worries are a common cause of relationship breakdowns.

One of the most common questions I get asked is, “What can I do with my money?” My immediate reply is always, “What do you want your money to do for you?” In other words, you need to decide first.

Getting started

Start the first month’s 15-minute session by just getting organised and making sure you both know where all your financial documents are kept and whether they’re up to date.

Collect all the insurance policies (life, disability, health, home and contents etc), check the cover is still right for you (if not shop around for alternatives) and put them in the one place where both of you can easily access them.

The same with mortgage documents, superannuation accounts and reports, bank documents, investment records as well as tax returns and receipts.

Then there’s the will. No-one likes talking about the possibility of death but the prospect of leaving your family in the financial lurch is just plain stupid. Read each other’s wills and make sure they’re current and relevant.

Just knowing where your financial documents are stored and what’s in them is a great start.

Another 15-minute session should look at your investments. Have you accumulated too many bank accounts? Could you earn more interest and pay fewer fees by consolidating them?

Are you in the right superannuation investment option that matches your risk profile and stage of life? Is it time for both of you to visit a financial planner to talk about an investment plan?

Playing the financial future game

Once you’re both on top of your financial position, it’s time to think about the future, what you each want from it and how to afford it.

Here’s how to do it:

First up, put your phone on silent, put the kids to bed, clear off two horizontal surfaces (preferably not too close) and gather lots of blank paper and coloured pens/pencils.

Individually answer these questions and write the results down under three headings:

What do I NEED in the:

next 12 months

next five years

when I retire

then,

What do I WANT in the:

next 12 months

next 5 years

when I retire

It helps if you have planned for this exercise and given it some thought.

Don’t hold back on what you want. Better to let your partner know now that you’ve always wanted a rural cottage, with chooks and a couple of horses, before they get too settled in that post-retirement inner-city terrace of their dreams!

This is your ultimate wish list.

‘Needs’ are necessities. Things like rent or home mortgage payments, food, council rates, electricity and gas … you get the drift.

‘Wants’ are dreams and the little extras. Things like dining out, entertainment, holidays, car. This list should only be limited by your expectations and goals.

Remember now is the time to disclose those burning ambitions and secret purchasable desires.

Prioritise your ‘Wants List’, with the top of the list being what you want most and the bottom being what you can most probably do without.

Then it’s show and tell time. You show me yours and I’ll show you mine.

Surprise, surprise! Shock horror? Or are you both on the same track? Sharing the Wants List is usually the eye-opener. It’s highly likely there will be some surprises there.

So now discuss your wants. Discuss, but take care not to be judgmental of your partner’s ideas. This is not the time to ridicule any idea. These lists will form part of your budgeting and, like all good budgets, they are not written in stone. They will need to be reviewed at very regular intervals and can be changed as your wants and needs change.

Start tonight. 15 minutes a month is not a lot to ask to think about your financial future.

Tell me how you go.