- Your Money & Your Life

- Posts

- My budget thoughts + Is the US market at it's peak

My budget thoughts + Is the US market at it's peak

My Money Digest - 15 May 2026

David Koch

May 15, 2026

Hi everyone,

I hope you’ve survived federal budget week. You’re probably sick of the wall-to-wall analysis so I’ve kept my snapshot short and sweet.

My big takeaways are the cost of living squeeze on household budgets is not going to ease and the best places to invest are going to be your home (which remains capital gains tax free) and your superannuation (where returns are concessionally taxed).

Also, negative gearing isn’t completely dead. You can still borrow to invest in shares, ETFs or managed funds and claim full interest deductibility against your salary. Borrowing against your home equity - with home loan interest rates around 5.5–6.5 per cent - while retaining full interest deductibility is an interesting option.

Having said that, I think people can get too carried away with the tax consequences of investing. The number one priority should be choosing the investment with the best potential long-term returns. Any tax concessions should be viewed as icing on the cake rather than the primary motivation.

This week’s newsletter:

The federal budget’s forecast for your financial life.

The tax reform centrepiece explained.

Government debt is low, but household debt is extreme.

Putting interest rates into perspective.

The private health insurance hit for older Australians.

Rents continue to surge.

Financial fragility and the $500 emergency buffer.

Super fund returns bounce back.

Is the US sharemarket close to its peak?

The budget’s forecast for your financial life

The next 12 months will continue to be tough for Australian households. The cost of living crisis will continue, wages won’t keep pace with inflation, interest rates will stay higher for longer and while the economy will slow, it won’t dip into economic recession.

But our jobs are secure.

That’s the helicopter view of your financial life over the next 12 months from the federal budget.

While it bombards us with data and new policies, the budget is simply a blueprint for your financial life over the next year. And it doesn’t appear that things are going to improve financially anytime soon.

Economic growth will slow to a meagre 1.75 per cent next financial year before it improves to a more normal 2.5 per cent the year after.

Here’s a snapshot:

Your job

Unemployment has remained impressively low over recent years as job creation has stayed strong. This is mainly because of record government spending on infrastructure and energy transition projects.

Unemployment, according to the budget forecasts, will stay around 4.5 per cent despite a slowing economy.

Nominal wages growth is expected to remain above 3 per cent, and annual real wage growth will return from next year, after growing for eight of the last nine quarters.

But with inflation peaking at 5 per cent and nominal wages above 3 per cent, real wages will go backwards through the peak inflation period before turning positive again from 2027.

Your family budget

Real wages are expected to decline through the peak inflation period before turning positive again from 2027. Petrol relief is also temporary, with the 26.3 cents-per-litre fuel excise cut and the reduction in the heavy vehicle road user charge both scheduled to end by July.

Income tax cuts will flow to more than 13 million workers, with the 16 per cent tax bracket reducing to 15 per cent from 1 July — delivering an average tax cut of around $50 per week compared with 2023–24. The new $1,000 instant tax deduction, which does not require receipts, is expected to save 6.2 million taxpayers an average of $205. Energy rebates of $150 for households will also continue.

With the RBA likely to tighten further as inflation peaks before cuts resume from 2027, variable mortgage costs are expected to rise before falling. This burden will be felt disproportionately by younger households.

Overall, lower and middle-income working households will be modestly better off through tax cuts, while mortgage holders and families affected by NDIS changes will be worse off. Aspiring home buyers, however, may be structurally better positioned.

Your house

The budget doesn't publish a headline dwelling price forecast (Treasury rarely does), but the relevant supply assumptions are:

65,000 additional new homes over the decade are expected to be enabled through the $2 billion enabling infrastructure fund, on top of the existing 1.2 million homes target.

75,000 Australians estimated to be helped into home ownership via the CGT and negative gearing changes (Treasury modelling).

Construction of government-built homes is expected to commence from 2026–27 under the Housing Australia Future Fund pipeline.

The bigger story for house prices is the demand-side tax reform: replacing the 50 per cent CGT discount with indexation, limiting negative gearing to new builds, and introducing a 30 per cent minimum CGT rate.

These changes are prospective from July 2027 with grandfathering, so the near-term price impact in 2026–27 is likely modest, although expectation effects on investor demand could be material from the time of announcement.

Your small business

The package is genuinely supportive and represents the most coherent small business measures in years.

Permanent measures:

$20,000 instant asset write-off made permanent (removing the annual uncertainty that has plagued planning since 2015).

More dynamic tax instalments (cashflow-friendly).

Simpler tax-time compliance, saving an estimated 376,000 hours annually across the sector.

Tax reform: the budget centrepiece explained

This is the most significant personal/capital tax reform package since the early Howard years:

Capital gains tax discount replaced with inflation indexation. The 50 per cent CGT discount is being replaced with inflation-adjusted indexation to restore the taxation of real gains.

New builds retain the option to use the 50 per cent discount. This is a genuinely substantive structural reform - taxing real rather than nominal gains is more defensible economically than the blunt 50 per cent discount, though the revenue impact depends heavily on inflation outcomes.

Negative gearing limited to new builds from July 2027, prospectively.

30 per cent minimum tax on capital gains and discretionary trusts. A minimum 30 per cent tax rate on capital gains from July next year, and on discretionary trusts from July the year after, to better align taxes on these income types with taxes on wages.

Workforce tax cuts funded by the above measures, with new revenue returned to workers and businesses over the next four years and tax relief for over 13 million workers.

A $1,000 instant tax deduction without receipts, affecting 6.2 million taxpayers and saving an average of $205, alongside a permanent $20,000 instant asset write-off for small business.

Source: Coolabah Capital

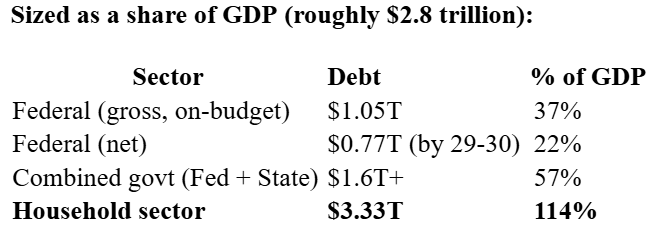

Government debt under control ... but we should be more worried about household debt

I know there is a lot of commentary and panic around the size of government debt, and the fact that gross debt will pass $1 trillion in the next financial year.

Yes, it’s a big figure but Australia is a big economy.

Think of the economy as your house. The debt/mortgage is 37 per cent of the value of the economy/house. That is manageable.

Despite all the hysteria around government debt, here are the facts. We have low government debt and extreme household debt:

Household debt is approximately three times the size of Commonwealth gross debt, and roughly twice the size of total combined government debt in Australia.

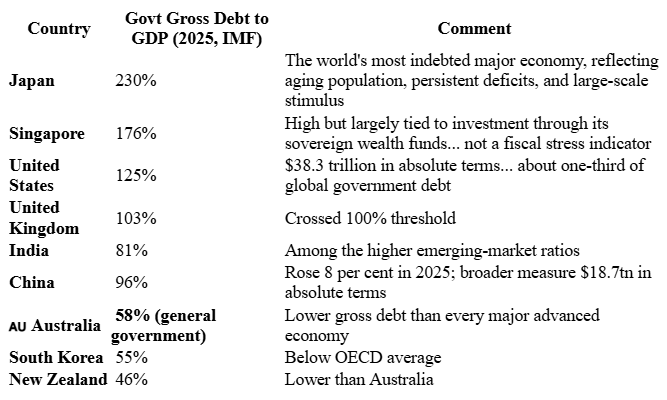

Now let’s compare Australia's debt with our top eight two-way trading partners: China, Japan, United States, South Korea, India, Singapore, New Zealand, and the United Kingdom.

The International Monetary Fund measures general government gross debt (which captures all levels of government) and puts Australia at around 58 per cent for 2025:

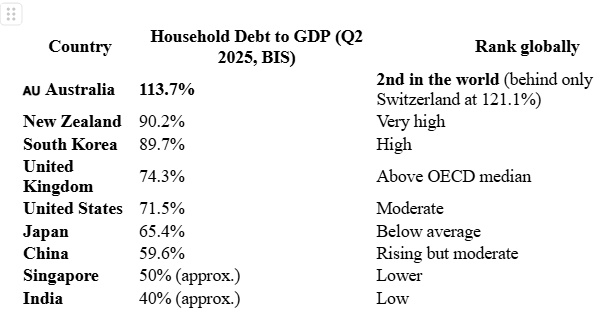

Household debt comparison

When it comes to household debt, the picture flips entirely.

The Bank for International Settlements (BIS) Q2 2025 data shows Australian households as among the most indebted in the world.

Australian households carry more debt relative to GDP than all eight major trading partners. It is roughly 1.6 times that of the US, 1.7 times Japan’s, and 2.9 times China’s as a share of GDP. The only major Western countries above Australia globally are Switzerland, Canada, and the Netherlands.

Hopefully that clears up the debt situation.

Now, let’s look at the economic and government policy implications of low government debt but extreme household:

Monetary policy (interest rate) movements are unusually powerful. With household debt at 114 per cent of GDP and a high share of variable-rate mortgages, every RBA rate rise hits domestic demand harder than in the US, UK or Japan, where households are less geared and often hold long-term fixed-rate mortgages. The budget's assumption of rising rates through the inflation peak, implies consumer demand will be hit harder than other economies.

Fiscal space is real but politically expensive to use. Australia genuinely has fiscal headroom that Japan, the US and the UK do not. But the reason government debt is low is that the private sector (chiefly households via mortgages) has done the borrowing instead. Stimulus into a household balance sheet already carrying debt of around 114 per cent of GDP doesn’t translate into increased household spending, because marginal income is often directed toward debt repayments rather than consumption.

Tax reform is a lever. The housing tax reforms in this week’s budget make more sense in this context. Replacing the CGT discount with indexation and limiting negative gearing aren’t just revenue measures - they’re structural tools aimed at slowing the growth of household debt, which is now the dominant financial risk to the economy. The Reserve Bank can’t address this through interest rates alone; only tax and supply-side policy can.

Sovereign rating logic. Despite household debt at 114 per cent of GDP, Australia retains a AAA sovereign rating from all three major agencies. This is because sovereign ratings assess the government’s ability to pay, and a low public debt burden alongside a wealthy private sector (even if highly leveraged) is considered highly serviceable. Rating agencies’ greater concern is typically state-level finances rather than the Commonwealth.

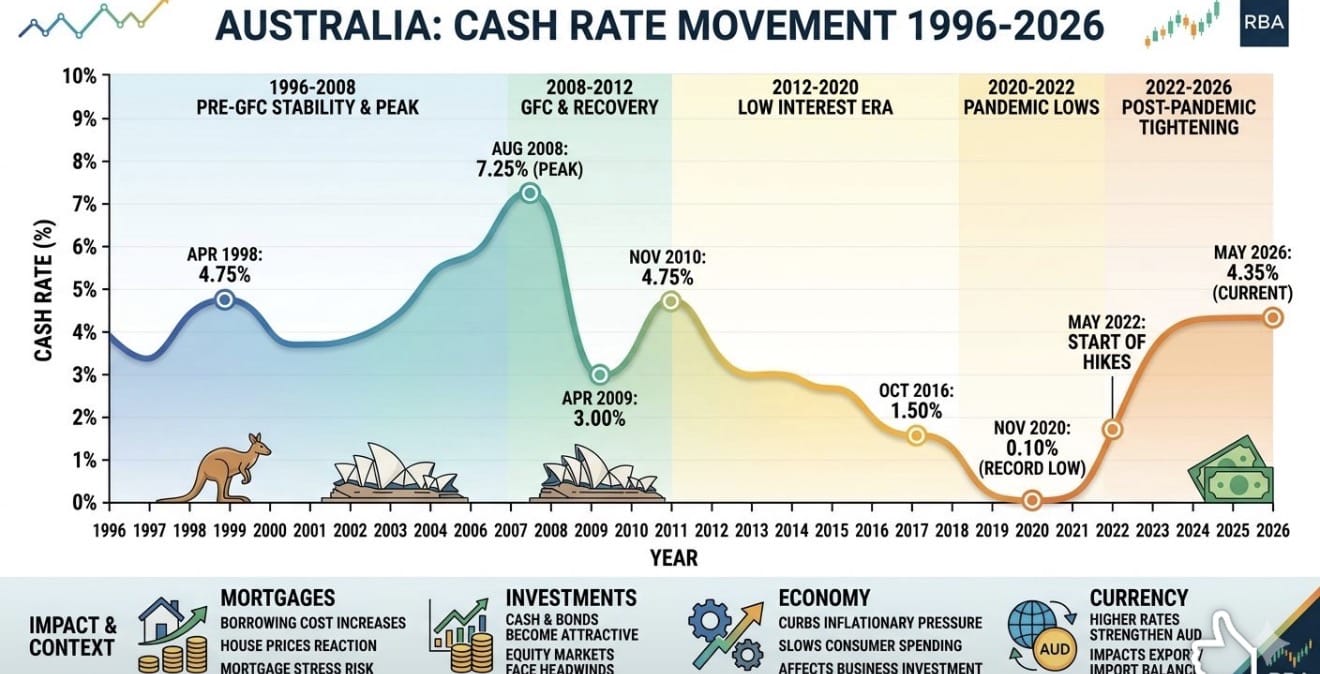

Interest rates in perspective

With the federal budget’s economic forecasts indicating interest rates are likely to stay higher for longer, it’s interesting to look at how current rates compare with the last 40 years:

Source: RBA

Private health insurance hit for older Aussies

More than three million older Australians - including more than 400,000 pensioners with private health insurance - will be hit by the Albanese Government’s decision to cut private health insurance rebates for Australians aged over 65.

Private Healthcare Australia warned the decision would force millions of retirees to pay hundreds of dollars more each year to keep their cover, place additional pressure on public hospitals, and threaten the viability of some regional private hospitals that care for large numbers of older Australians.

From April next year:

Australians aged 65–69 earning under $101,000 as a single or $202,000 as a family will see their rebate reduced from 28 per cent to 24 per cent.

Australians aged 70 and over in the same income brackets will see their rebate reduced from 32 per cent to 24 per cent.

The changes come on top of inflation driven annual premium increases which averaged 4.4 per cent this year but were higher for comprehensive Gold products.

Private Healthcare Australia said the impact would fall hardest on retirees living on fixed incomes, including pensioners and part-pensioners who have maintained private health insurance for decades to ensure timely access to healthcare with their own choice of doctor, and to reduce pressure on the public system.

Rents continue to surge

My big worry with the capital gains tax and negative gearing changes is that property investors will just think it’s just getting too hard to be a landlord and invest elsewhere.

That could mean more properties become available for first home buyers but it also means less properties available for renters.

Rents are currently rising strongly and a worsening shortage of available rentals will exacerbate the issue.

According to SQM Research, national advertised rents continued to rise through May, with combined rents increasing 0.7 per cent over the past 30 days and 7.3 per cent higher year-on-year, reflecting ongoing tight rental market conditions across most capital cities.

The national combined rent average now stands at $696.94 per week, while the capital city average has increased to $794.54.

Nationally, house rents rose 0.5 per cent for the month and 7.8 per cent over the year, while unit rents increased 0.8 per cent monthly and 6.5 per cent annually.

City rental snapshot:

Sydney: Combined rents rose 0.3 per cent for the month and 7.3 per cent year-on-year, with house rents averaging $1,156.97 per week.

Melbourne: Combined rents increased 0.3 per cent monthly and 6.1 per cent annually.

Brisbane: Combined rents rose 1.4 per cent for the month and 8.1 per cent over the year, reflecting continued population-driven demand.

Perth: Combined rents declined 0.2 per cent over the month but remain 6.3 per cent higher year-on-year, indicating some short-term easing after sustained growth.

Adelaide: Combined rents fell 0.8 per cent for the month but are still 4.6 per cent higher annually, with unit rents continuing to outperform houses.

Source: SQM Research

Financial fragility and the $500 emergency bill

Picture this: one of those weeks where everything goes wrong at once. The car battery dies, a sudden toothache turns into an emergency root canal, school camp fees hit your inbox, and the dog eats something he shouldn’t …

Then, as you tap your credit card, this time to pay the vet, you hesitate. Expenses have piled up and the total is climbing faster than you can breathe.

Now ask yourself: Would I have savings to cover just one or two of these things?

If you answered ‘no’, you are not alone.

Living pay cheque to pay cheque

For a growing number of Australian households, financial security is far more fragile than it appears.

Data suggests even an unexpected $500 expense is enough to push a significant portion of us into debt. Research from Compare the Market where I am Economic Director, shows a significant share of Australians have little to no savings, with more than 20 per cent saying their savings are going backwards.

It’s not hard to see why. Interest rate rises, persistent inflation and volatile fuel prices are

putting sustained pressure on household budgets - it’s crushing, actually.

In this environment, unexpected costs aren’t just inconvenient, they’re devastating and destabilising, eroding financial stability before we can course correct.

Crunching the numbers on credit

Without a little cash set aside, these unexpected expenses often end up on credit cards,

personal loans or Buy Now, Pay Later services.

What starts as a $500 problem can quickly become much more expensive once interest and fees are added.

Consider a typical scenario:

$500 charged to a credit card

Interest rate: ~20% p.a.

Minimum repayments: ~2–3%

What happens next:

It can take two to three years to repay

The total cost can rise to $600-$700+

That’s $100 - $200+ in interest for a single small expense

And these numbers do not account for existing debt. For many Australians, new expenses are added on top of credit balances - compounding the problem further.

With around half of Australians already carrying credit card debt, the risk of a short-term

setback turning into long-term financial strain is very real.

Which is exactly why an emergency fund matters more than ever in this economic climate.

Saving for surprise expenses

An emergency fund is exactly what it sounds like: a pool of money set aside specifically for the unexpected. It’s not for everyday spending or a holiday, it’s there to absorb life’s shocks without forcing you into debt.

Even a modest buffer can make a meaningful difference.

Having $500 to $1,000 set aside can stop emergencies from spiralling into long-term financial stress. A surprise bill isn’t really the problem, it’s what happens when you have no choice but to borrow to cover it.

Building a buffer when money is tight

Saving money right now is hard, I know. And telling people to simply “save more” is eye-rolling. But here’s the thing, building an emergency fund is one way to relieve this cost-of-living pressure.

Having a little money set aside for emergencies, covers you, so these don’t grow into out-of-control debt. Think of it as insurance for ‘bad weeks’.

Start small, say with a $500 goal. That’s often enough to handle minor surprises without

turning to credit. From there, you can build it towards $1,000 - and so on.

Here are few practical ways to raise the cash to get started:

Keep it separate: Open a dedicated savings account so the money isn’t easily spent.

House it in an offset account: If you have one, an offset account is the perfect home for an emergency fund as the interest earned goes against your home loan and is easily drawn down.

Save what you can: Even $10-$20 a week adds up over time.

Trim where possible: Use your car a little less (and save $50 a week), pause a subscription, or cut back temporarily in one area - say Friday night drinks.

Sell unused items: Turn things you don’t use into cash to kickstart or boost your buffer.

Capture windfalls: Put tax refunds, rebates, tips or bonuses straight into the emergency savings account before they’re spent.

Automatic debit on payday: Set up a fixed amount to be automatically transferred each month. Over time, it becomes an “invisible” transaction you barely notice.

Top up the fund: If you need to dip into the emerging fund, be committed to rebuilding it ASAP - before you are back to being in a risky credit position.

Think of building up your emergency fund as a crash diet... it’s only for a short period while you get your stash to the first $500 or $1,000. Rigid restricting of your spending for any long period will likely lead to blowouts and failure. Falling off the wagon, as they say.

But once it’s in place, you can loosen your belt a little.

Pre-empting a bad week

The reality is, cars break down. Kids need things. Health issues arise. Appliances fail at the worst possible moment.

Without a buffer, a bad week can linger for months or even years in the form of repayments, interest and financial stress. With even a small emergency fund, that same week becomes something you can absorb, recover from, and move on.

A $500 problem doesn’t turn into a $5,000 one.

Because your emergency fund has you covered.

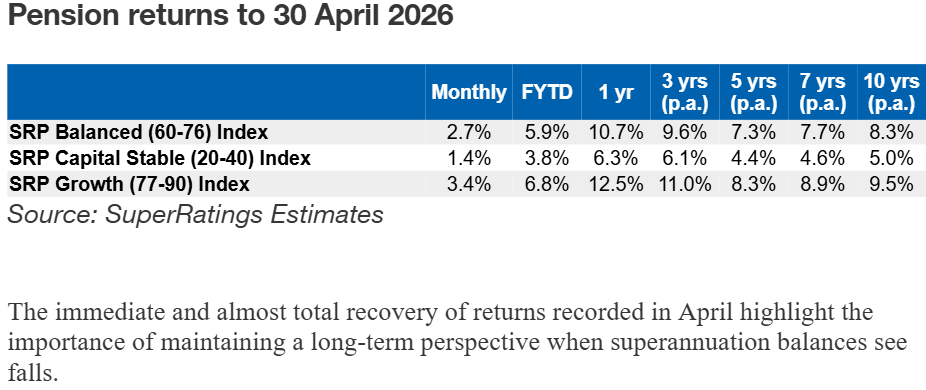

Super fund returns bounce back

The announcement of an uneasy US–Iran ceasefire in early April helped drive some recovery in markets and benefited super fund returns in April.

Leading superannuation research house SuperRatings estimates a gain of 2.6 per cent for the median balanced option over the month of April, recovering much of the 3.2 per cent loss recorded in March.

The median growth option gained an estimated 3.1 per cent over the month, while the median capital stable option is estimated to have gained 1.3 per cent.

Pension returns experienced a similar recovery in April, with the median balanced pension option achieving an estimated return of 2.7 per cent, compared to the March loss of 3.6 per cent.

The median capital stable pension option is estimated to have risen by 1.4 per cent over the month, while the median growth pension option is estimated to have risen 3.4 per cent over the same period.

The immediate and near-total recovery of returns recorded in April highlights the importance of maintaining a long-term perspective when superannuation balances experience falls.

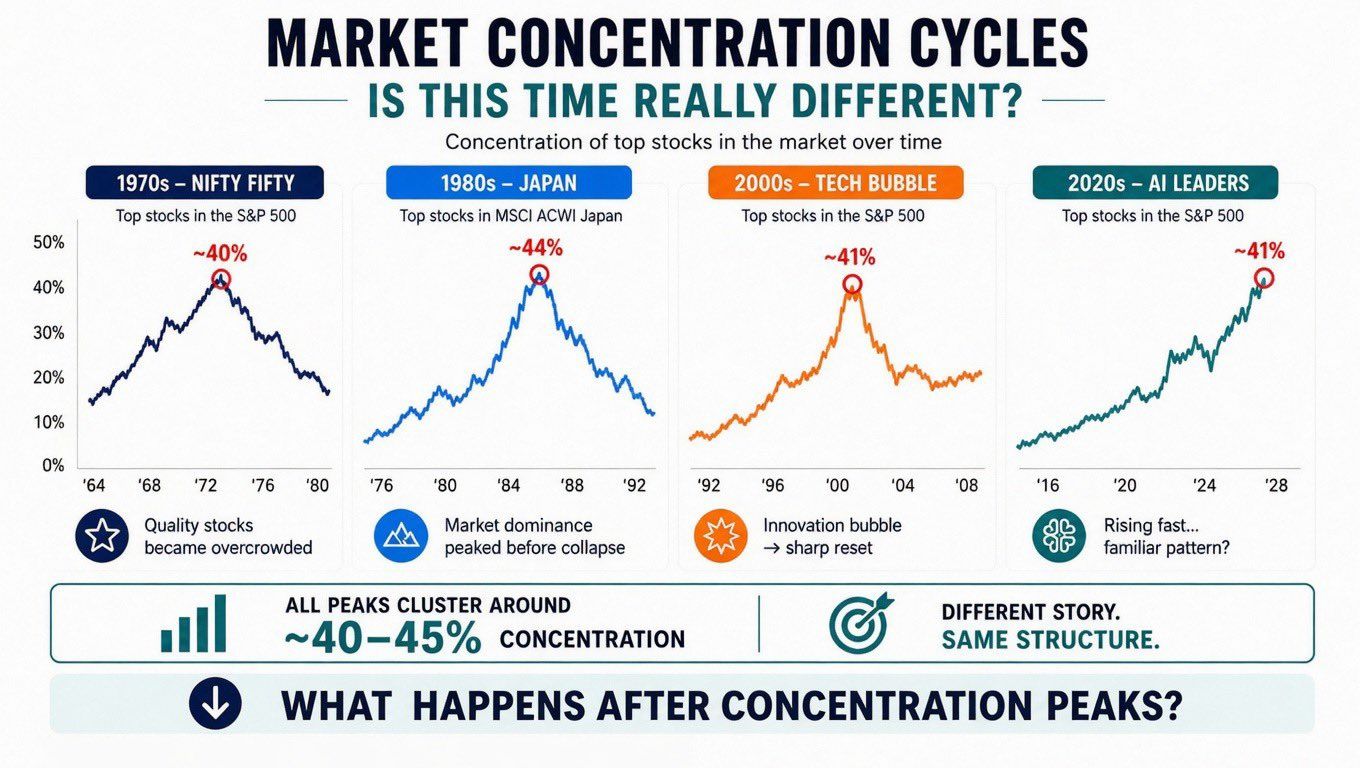

Predicting the future of sharemarkets is always fraught with danger. But there is a growing list of investment gurus who are concerned that the US sharemarket continues to break record highs, despite Middle East tensions, skyrocketing US debt and a slowing American economy.

Given these concerns, I thought this chart below was fascinating. It focuses on when markets are driven by a concentrated number of leading companies, which creates the peaks but also signals a possible downturn to follow.

Source: Bank of America