- Your Money & Your Life

- Posts

- Give yourself a rate cut + Why this government scheme is good for some

Give yourself a rate cut + Why this government scheme is good for some

My Money Digest - 03 October 2025

David Koch

October 03, 2025

Hi everyone,

Welcome to October. Daylight saving starts for most states this weekend and we go to this crazy situation where instead of three time zones we have five.

From a financial point of view, it has been a little crazy this week with a lot of uncertainty about future interest rate cuts. A lot to talk about so let’s get stuck into it.

In this week’s newsletter:

RBA keeps rates on hold... and may stay that way for longer.

Don’t wait for the RBA. Here’s how to chase your own rate cut.

While rates are on hold, your home keeps rising in value.

The housing shortage is set to continue.

Why the First Home Guarantee is good for renters.

Small cap stocks set for a turn around.

How the world’s energy is being produced.

RBA keeps rates on hold as expected ... and may stay on hold for a while

No surprises that the Reserve Bank kept official interest rates on hold last Tuesday at 3.6 per cent. But the expected rate cut on Melbourne Cup Day in November is now in doubt.

The higher-than-expected monthly CPI figures for July and August have spooked the RBA, raising concerns about whether inflation is truly under control. They were always likely to wait until the more reliable September quarter CPI, due in late October, before making any decisions on changing interest rates.

The first heading in the RBA’s statement read, “The decline in underlying inflation has slowed” ... which doesn’t engender great confidence.

Given the cautious and gradual easing cycle so far, the RBA will want to wait to see evidence that inflation continues to head towards the mid-point of the 2-3 per cent target band before easing them further.

This is why why economists, including the Commonwealth Bank are now forecasting rates will stay on hold until the February board meeting, and after the December quarter inflation result.

Governor Michele Bullock noted in her press conference that the RBA is aiming for inflation to return to 2.5 per cent. Inflation remaining above this target over the forecast horizon won’t be enough to trigger a cut.

The press conference also highlighted the RBA is watching inflation developments offshore. The Governor highlighted sticky services inflation offshore and this could be giving the Board food for thought.

Overall though the press conference highlighted how uncertain the RBA is of the outlook. The decision to leave the cash rate was unanimous, unlike at the July ‘on-hold’ decision where the Board was split 6-3 ahead of the August rate cut.

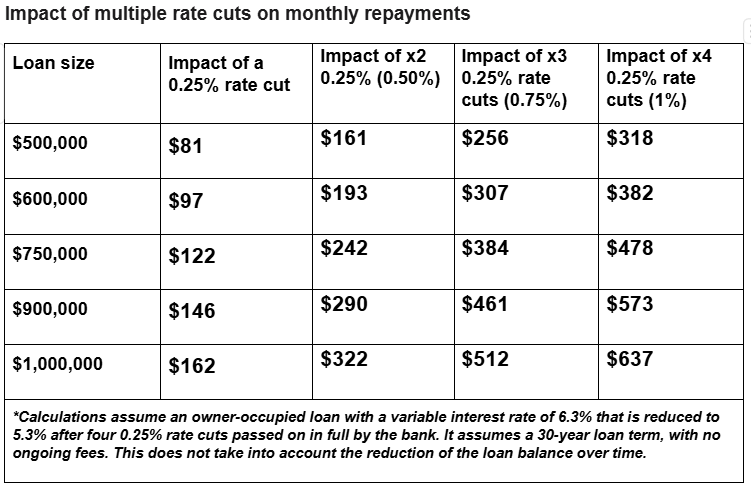

Don’t wait for the RBA - you can chase your own rate cut

Many homeowners can start saving regardless of what the RBA does. The average interest rate for outstanding loans is 5.76 per cent. Right now, there are variable rates from 5.34 per cent - that could be a saving of about $179 a month, surpassing what a typical RBA cut would deliver.

There are even two-year fixed rates as low as 4.79 per cent. That’s the lowest we’ve seen in years and could be a smart option if you’re looking to start saving now and lock in some certainty for the months ahead.

If you think inflation is going to stay stubbornly high and the RBA will keep rates on hold for a considerable time, then this two-year fixed rate could be attractive as part of a loan cocktail to provide some certainty. It’s the equivalent of four 0.25 per cent rate cuts below the average variable loan rate today.

More Australians are taking power back into their own hands by comparing and switching to cheaper rates. Around 65,000 home loans were refinanced by borrowers moving to different lenders in June, a 25 per cent increase on the previous year. And 43,000 loans were refinanced with their existing lender. In other words, borrowers contacted their lender, asked for a better deal, and got one.

A good broker can help you do the leg work and negotiate a great rate on your behalf.

Source: Compare the Market

While home loan rates are on hold, the value of your home keeps rising

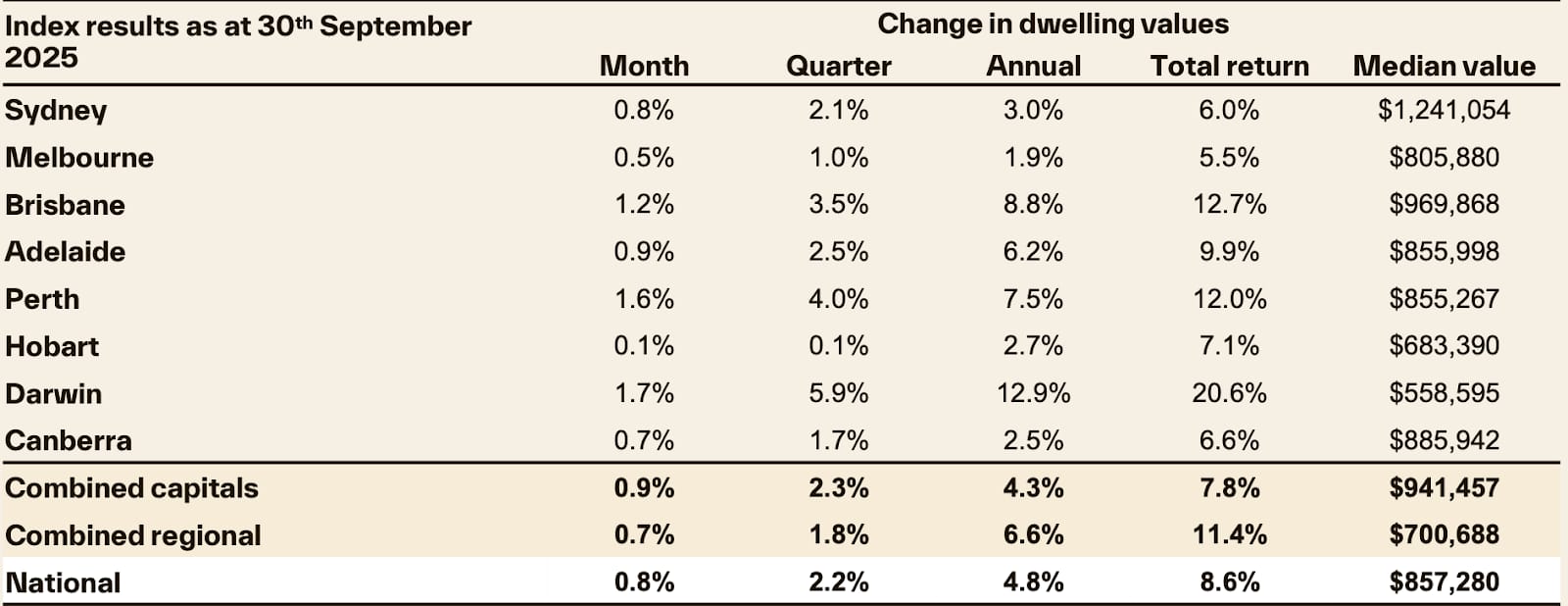

Australian housing markets are gathering strength as we head further into spring, with September marking the strongest monthly gain for national dwelling values since October 2023. That’s according to Cotality’s Home Value Index (HVI) which recorded a 0.8 per cent increase in September, powered by 0.9 per cent rise in capital city values.

On a quarterly basis, the national HVI increased 2.2 per cent, up from a 1.5 per cent lift in the June quarter and double the 1.1 per cent increase seen over the three months to March.

Growth has once again become broad-based, with every capital city and rest-of-state region recording an increase in dwelling values over the month, quarter and most recent 12-month period.

Perth and Brisbane are again pulling ahead of the larger capitals, with values up 4 per cent and 3.5 per cent respectively through the September quarter, with the pace of gains being led by the home unit market. Darwin is showing an even stronger run of growth with values jumping 5.9 per cent higher over the past three months.

Most cities are seeing stronger growth rates for houses than units, with capital city values up 2.4 per cent and 1.7 per cent respectively through the September quarter. However, in Brisbane, unit values are consistently rising at a faster pace than house values over the past seven quarters due to a severe supply shortage. Perth and Hobart have also seen unit values outpace houses in the September quarter, though this trend has been less consistent than in Brisbane.

Advertised stock levels are below average across every capital city adding to the momentum in home value growth. Over the four weeks to 28 September, capital city listings tracked about 18 per cent below the previous five-year average.

Source: Cotality

Housing shortage to continue

At RBA Governor Michele Bullock’s press conference after the interest rate decision, she was asked whether interest rate cuts were fuelling the housing boom and contributing to the crisis.

She was pretty blunt in arguing it’s the lack of building new houses that is the problem ... not interest rates. And she doesn’t believe the housing shortage will be solved for a number of years.

The August building approvals figures released this week support the RBA Governor’s argument and highlight the failure of government initiatives to build more. Instead, the new broader 5 per cent deposit scheme just adds to demand and does nothing for supply.

The total number of Australian dwellings approved fell by 6 per cent in August to a 12-month low. Approvals are up 3 per cent compared with a year ago, the weakest annual pace since June 2024.

Council consents for private houses slid 2.6 per cent to an eight-month low of 9,027 and for private dwellings, ex-houses (apartments) approvals dropped 8.1 per cent to a four-month low of 5,408.

The annualised rate of building approvals increased to 187,691 in August, the highest level since January 2023, remaining well below the federal government’s building target of 240,000 homes per year.

The Australian federal government has an ambitious target of 1.2 million new homes by 2029. That looks impossible to achieve.

By state and territory in August, approvals for total dwellings were down across most states: Victoria (down 11.8 per cent), NSW (down 11.4 per cent), South Australia (down 10 per cent), and Western Australia (down 7.3 per cent) all fell. Tasmania (up 14.4 per cent) and Queensland (up 3.7 per cent) both rose in August.

The First Home Guarantee … the missing issue

I’ve talked about the Federal Government’s expanded 5 per cent home deposit loan quite a bit. Like the wider media commentary over the last few days, and earlier in this newsletter, I’ve made the point that while it allows easier entry for first home buyers into a home, it won’t solve the housing crisis.

The only solution to the housing affordability crisis is to, as I’ve already mentioned, build more housing.

If anything, the First Home Guarantee it will add to demand for property and push up values further. Borrowers also have to be careful not to overextend themselves. Lower deposit means a bigger loan and higher interest payments over the term of a loan.

BUT what none of the media coverage has pointed out is that any extra costs from a bigger loan could be offset by what First Home Buyers will save on rent. Not only is Australia in the middle of a housing crisis but also a rental crisis. A shortage of rental properties has been pushing up rents so much that it has been a big inflation driver.

Taking advantage of the First Home Guarantee gives a young Australian the chance to swap that rent for their own home... yes, it will come with a big loan and repayments, but it is also a strongly appreciating asset and they are building significant equity in that asset.

Property research group Cotality has done the numbers and the outcome is fascinating.

Since the scheme’s introduction as the ‘First Home Loan Deposit Scheme’ in January 2020, rising rent costs have put the scheme in a new light. Since January 2020, the median weekly rent across Australian dwellings has increased an estimated $200 per week, to $669. That’s an uplift of over $10,000 per year.

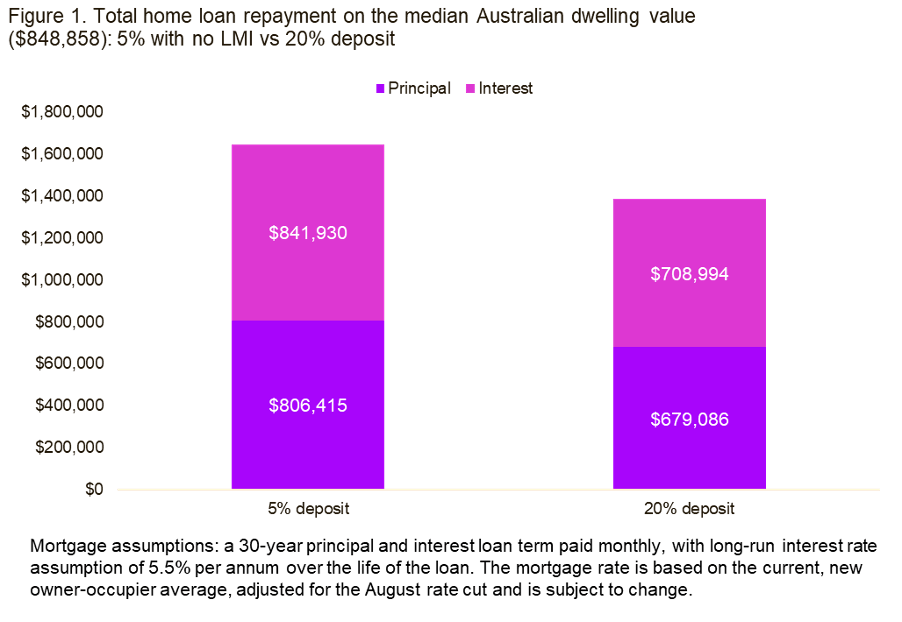

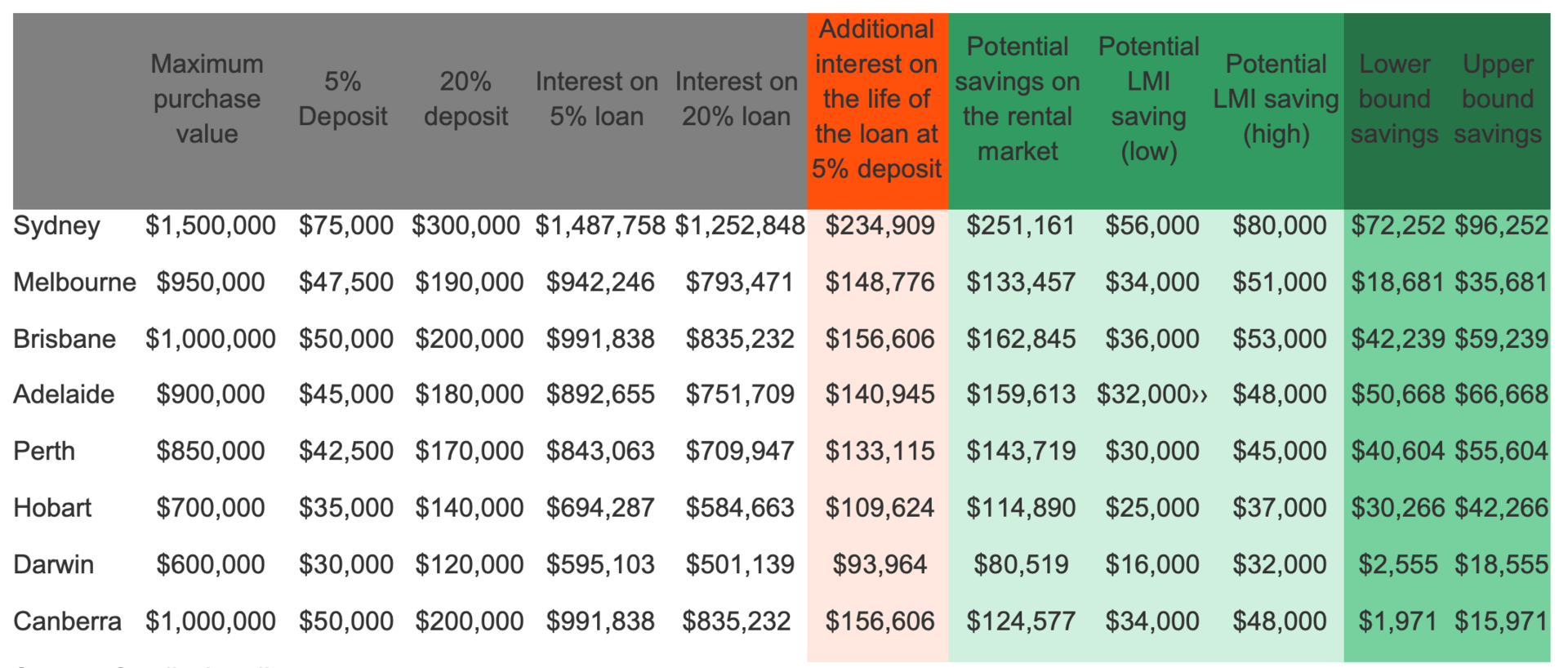

According to Cotality, first home guarantee schemes comes at a cost, both to individuals who take them up, and the broader housing system. The main cost for individuals is extra interest paid over the life of a loan. The flipside of a 5 per cent deposit on a home purchase is a 95 per cent loan to value ratio (LVR) on the home loan. Taking out the extra debt means paying extra interest compared to the traditional 20 per cent deposit. This chart shows an example based on the median dwelling value in Australia.

Source: Cotality

Over the life of a 30 year loan, the extra interest costs can be tens of thousands, or hundreds of thousands more than a 20 per cent deposit home loan.

Even though a smaller deposit means paying more interest over time, it could still work out cheaper for renters. Getting into a home sooner may mean spending less time paying rent, and those savings can add up.

The biggest savings across the capital cities are estimated to be in Sydney, where a 5 per cent deposit reduces time to save a deposit by an estimated six years, and $251,000 on rent at $801 per week.

This table compares the additional interest cost of a 5 per cent loan with potential Lenders Mortgage Insurance and rental savings. In this scenario, purchasing at the top of the scheme works out better than spending extra time in the rental market to save up a 20 per cent deposit. In fact, the rental savings far outweigh the savings on LMI.

According to Cotality, someone who does not have rental costs might find it more beneficial to save up a full 20 per cent deposit, saving on both LMI and extra interest costs. But there are other considerations to take into account even for non-renters, such as entering the market sooner to get ahead of further potential market upswings.

Source: Cotality / Lendi

Small caps stocks set for a turnaround

Small cap stocks have been going through a real purple patch on the Australian sharemarket and out-performing the bigger end of town.

Small caps continue to offer compelling opportunities, according to Lucas Goode from Investors Mutual who was interviewed this week on the ausbiz business and markets streaming channel (www.ausbiz.com.au and on SevenPlus and Samsung smart TVs).

Goode remains positive on the small cap rally, emphasising that there is still significant room for growth within the sector. He highlighted the merits in seeking out overlooked stocks that may have been unfairly penalised, especially as market winners have become fully valued.

His 3 top small cap tips are:

Australian Clinical Labs (ASX:ACL); a standout in the pathology space. Despite its share price underperformance and some recent earnings pressure -attributed to government changes in test reimbursements and normalising post-COVID demand - Goode sees ACL as the best-in-class operator.

He suggests long-term growth drivers, such as a defensive ageing population and the potential for increased testing, remain firmly in place. Goode also sees potential upside from industry consolidation, with a possible merger between ACL and Helios being a value-accretive opportunity.

Equity Trustees (ASX:EQT) and HMC Capital (ASX:HMC) are also on Goode’s radar. He notes Equity Trustees is trading at a substantial discount despite its strong fundamentals, following ASIC’s civil action and broader sector challenges.

HMC Capital, once a market favourite, has suffered from sentiment-driven discounts, but Goode likes its diversified asset base and sees the current valuation as a low-risk opportunity.

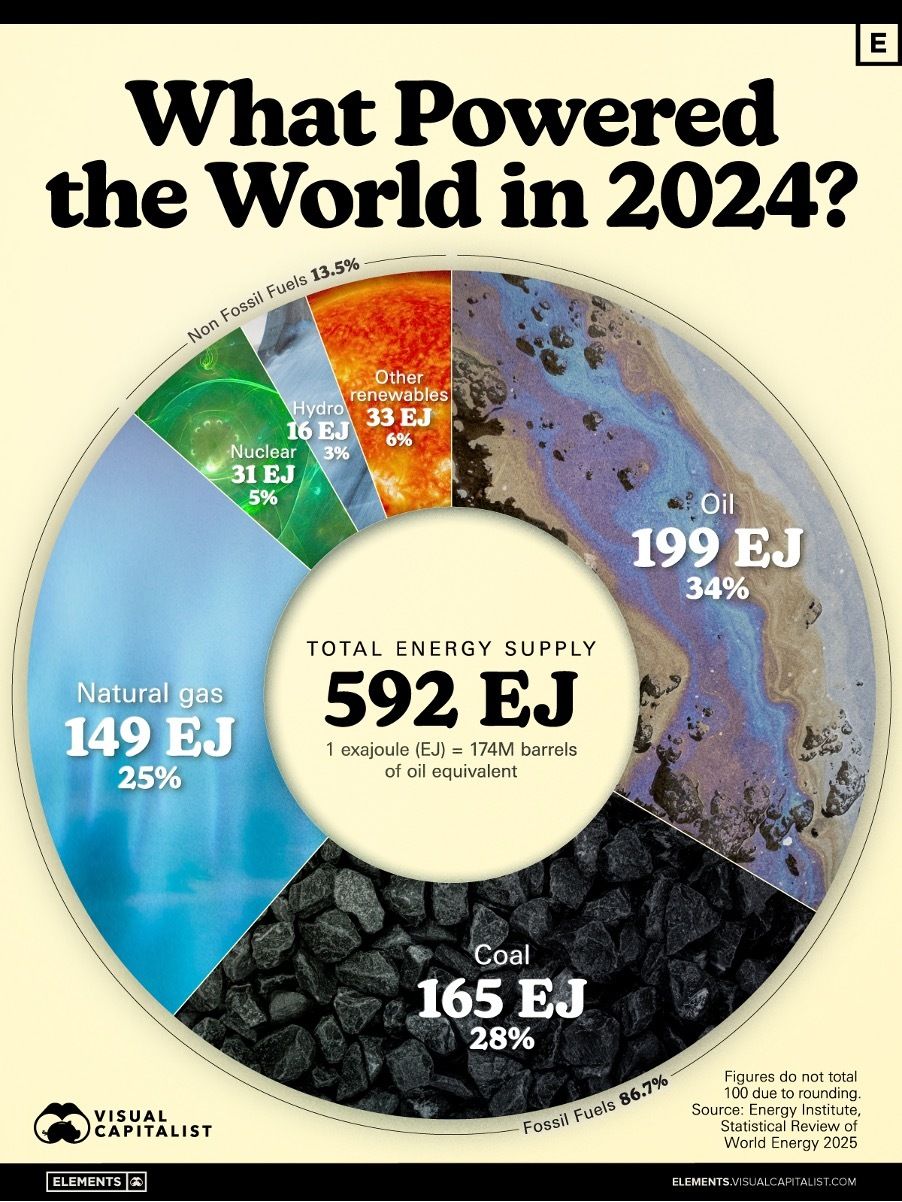

How the world’s energy is produced

Latest figures from the Energy Institute shows global energy demand increased 2 per cent in 2024 largely pushed ahead by the massive thirst from data centres and artificial intelligence chips.

The electrification of the global is a real thing which is why robust electricity grids will be more important than ever. So how is that electricity being generated?

Have a look at the chart below.

While cleaner technologies continue to expand, traditional energy sources still form the backbone of the global energy system. At the same time, the Asia-Pacific region drove 68 per cent of demand growth, reflecting the region’s rapid economic momentum and industrialisation.

Last year, oil, coal, and natural gas together supplied 86.7 per cent of global energy needs.

Oil remained the dominant energy source, accounting for 33.6 per cent of global supply. In 2024, average oil prices declined by 3 per cent, though they were still 27 per cent higher than in 2019.

Coal followed at 27.9 per cent, supported by increased consumption in emerging economies. Natural gas, though cleaner than coal, supplied 25.2 per cent, rounding out the fossil fuel trio.