- Your Money & Your Life

- Posts

- A super year for your savings + Trump and Venezuela explained

A super year for your savings + Trump and Venezuela explained

My Money Digest - 16 January 2026

David Koch

January 16, 2026

Happy New Year everyone,

I hope you’re enjoying a terrific summer holiday - it really is the best time of the year.

Libby and I had a perfect mixture of adventure and family time. At our age, you need to focus on ticking off bucket list experiences and enjoying the magic of a big, loud, diverse family.

Our summer highlights were:

Ticking Morocco off our bucket list, which lived up to our high expectations.

Visiting Georgie in London, seeing the Christmas lights and spending time with Heidi (#9 grandchild).

Spending Christmas with the Perth and Dubai branches of the family.

Skiing in Italy, visiting Berlin and being hosted by the parents of our son-in-law, Alex.

Celebrating New Year’s Eve in Paris, and ticking off seeing the Notre Dame restorations.

Visiting Sam and the kids in Dubai to see their new life.

And of course, returning home to meet grandchild #10, Valentina, for the first time.

It was a whirlwind but now it’s back on deck for 2026.

In this newsletter:

Property values losing momentum as interest rate realities hit.

Rents continue to rise well above inflation.

Why the Tax Office will be targeting holiday homes this year.

Another great result from your superannuation fund.

The stunning performance of gold ETFs.

Donald Trump’s reasons for controlling Venezuela in one chart.

What the banks are predicting for interest rates this year

There is so much speculation about ‘will we, or won’t we’ get an interest rate cut this year? Could rates go up instead, or will they just stay where they are for a prolonged period?

While the first Reserve Bank board meeting is on 3 February, a little over two weeks away, some of the big banks are already making their views clear by adjusting their fixed-rate home loans. These fixed-rate loans essentially reflect what banks predict interest rates will be in the future.

Australia’s biggest home lender, CBA, has lifted its three-year fixed rate by a whopping 0.70 per cent, from 5.34 per cent to 6.04 per cent. Its one-year fixed rate has risen by 0.45 per cent to 5.94 per cent, meaning the bank’s lowest fixed home loan rate is now 5.79 per cent for a two-year term.

CBA has also increased its four- and five-year fixed rates by 0.30 per cent, taking them to 6.09 per cent and 6.24 per cent respectively.

Macquarie Bank has also been moving its fixed rate loans again, adding 0.25 per cent.

Currently 34 lenders have hiked at least one fixed rate in the last month alone. So, the message is pretty clear from all the lenders: They’re expecting interest rates to rise in 2026.

To put this in perspective, a 0.25 per cent interest rate hike on a typical $600,000 mortgage would cause repayments to rise by $90 a month, on a $750,000 loan repayments would increase by $112, and a $1 million mortgage an extra $150 a month in costs.

Property values lose momentum, but 2025 still a great year

Cotality’s National Home Value Index recorded the smallest gain in five months, with values rising 0.7 per cent in December. This appears to reflect a growing realisation among potential buyers that no more rate cuts could be on the way.

Sydney and Melbourne were the biggest drag on the index, with values slipping 0.1 per cent. This marked the first month-on-month decline since January last year, prior to the rate cuts that commenced in February.

Every other capital city and region posted a rise in values through December, although most saw some momentum leave the market. A ‘higher for longer’ setting on interest rates, alongside a resurgence in cost-of-living pressures and worsening affordability pressures, looks to have taken some heat out of the market.

Despite the softer December outcome, the Home Value Index surged 8.6 per cent higher in 2025, adding approximately $71,400 to the national median dwelling value. This was the strongest calendar year gain in home values since 2021, with Darwin chalking up the biggest gain of 18.9 per cent and Melbourne the lowest at 4.8 per cent.

High-end properties are currently the weakest in the property market, with values across the most expensive homes rising just 0.2 per cent in December. By contrast, middle- and lower-value properties rose 1.1 per cent, driven by increased demand linked to the Federal Government’s 5 per cent deposit scheme.

Regional property values rose 9.7 per cent over 2025, outpacing the 8.2 per cent increase across the combined capital cities. Western Australia stood out with a 16.1 per cent annual increase, followed by regional Queensland, up 12.6 per cent. Regional Victoria recorded the lowest growth outcome over the year, with values up 6 per cent.

Source: Cotality

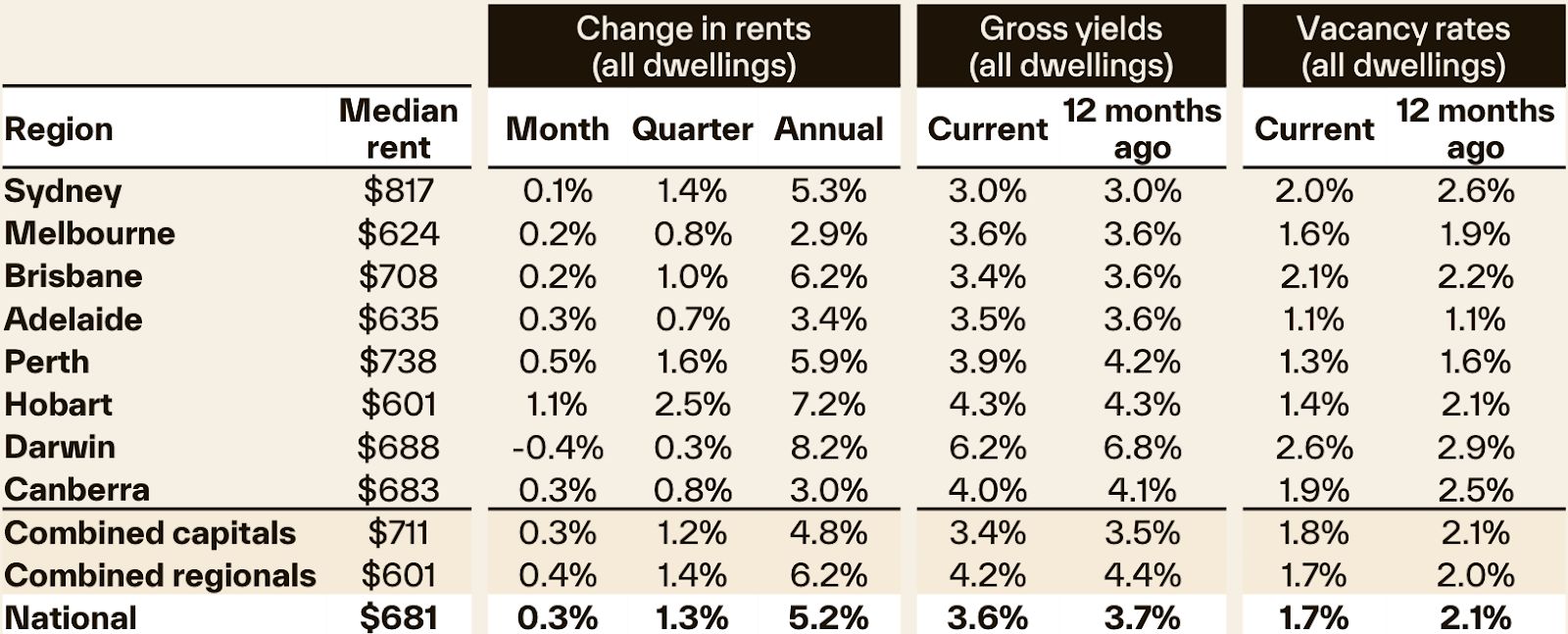

Rents continue to rise faster than inflation

While property owners had a good 2025, renters continue to be hit by rental increases well above inflation - and it appears the situation is getting worse.

Cotality’s latest Quarterly Rental Review measured a 1.3 per cent rise in national rents in the December quarter. This was up from 0.9 per cent in the September quarter. Over the full year, rental growth was 5.2 per cent - up from the 4.8 per cent in 2024.

If it’s any consolation, rents were climbing by more than 8 per cent a year between 2021 and 2023 - so the recent increases aren’t quite as dramatic. The main driver? Low housing supply. National rental listings were about 11 per cent lower than a year ago in the December quarter and 17 per cent down on the previous five-year average. It’s that old demand versus supply economic theory coming to the forefront yet again.

Vacancy rates also fell to 1.7 per cent, well below the pre-COVID decade average of 3.3 per cent, which shows just how tight the market is and how renters have to outbid each other to get a place - driving rent rises even more.

Regional property markets outpaced capitals, with rents up 6.2 per cent compared to 4.8 per cent across the combined capitals. Sydney remains the most expensive capital, with median dwelling rents at $817 a week, while Hobart is the most affordable at $601 a week.

Let’s not forget how these high rent increases feed into the inflation rate …

Source: Cotality

For those enjoying their holiday house …

Just a reminder that the Tax Office will be looking closely at your holiday home this year as new rules come into effect from July 1.

The ATO is proposing that certain holiday dwellings may be treated as ‘leisure facilities,’ preventing owners from deducting interest, rates or maintenance, unless the home is mainly rented to generate income.

So as you sit on the deck of your holiday house with a gin and tonic, start focussing on the fact that holiday homes in popular seasonal areas such as ski lodges or beach houses which are not available for rent throughout peak seasons will trigger ATO attention and may result in the denial of deductions.

Other triggers that will generate ATO interest may include:

Limited attempts to rent out the property.

Parts of the property being inaccessible for use by guests.

Pricing the property well above market rate to drive interest away from the property.

Renting the property to family or friends significantly below market rate.

The bottom line: make sure your property is truly available for rent, especially during peak season. Advertise widely, set a fair market rent, and avoid rules that can deter guests - like “no children,” “no pets,” or requiring references for short stays.

And, importantly, keep thorough records. Tax Office officials have always told me over the years that they win most disputes against taxpayers not on the merit of the case but because taxpayers don’t keep good enough records to substantiate their argument.

Superannuation has delivered another strong year of returns

Leading research house SuperRatings estimates that superannuation funds returned 9.1 per cent to members over 2025 for the median Balanced option - well above the long-term average of 7.1 per cent.

Investing in international shares was the key driver of performance throughout the year, although all asset classes made a positive contribution.

To close out the year, the median Balanced option (60–76 per cent growth assets) delivered a 0.35 per cent return in December. Positive returns in nine of the 12 months -highlighted by a stellar seven-month streak through to October - added up to a 9.1 per cent return for the 2025 calendar year.

Source: SuperRatings

The past three years of strong returns have lifted the long-term average for the median Balanced option to 7.1 per cent - well above the usual CPI + 3% target.

So when your annual super statement lands, the 9.1 per cent return for 2025 is a good benchmark. If your fund came in below that magic number, it’s worth asking why and checking if you’re with the right manager. Then look at the five and 10 year returns - they should be above 7 per cent.

The best performing ETFs for 2025

Precious metals, copper miners, and critical minerals were some of the best-performing assets in 2025, as investors turned to real assets amid geopolitical uncertainty, rising inflation, and the push toward electrification.

Gold-related ETFs led the way, with both gold miners and physical precious metals among the year’s strongest performers, driven by record price gains.

Gold finished the year 65 per cent higher at US$4,330 per ounce, while silver soared more than 150 per cent to US$72 per ounce - and that momentum is continuing. ETFs remain one of the easiest and most cost-effective ways to gain exposure to precious metals.

New Year resolutions ... what everyone else is doing

New year, new you - at least until the Instagram memes remind us that most resolutions are short-lived and barely make it past January.

But that doesn’t stop people from setting them. Research from Compare the Market reveals the resolutions Aussies are most determined to stick to in the year ahead.

It’s looking like 2026 will be the year of the health kick, with around a third of Aussies surveyed (37.50 per cent) saying they aim to live a healthier lifestyle next year.

The findings show that Millennials are the most likely to set resolutions focused on living healthier in 2026, with 43 per cent doing so, compared to 42 per cent of Gen X, 37 per cent of Gen Z, and just 30 per cent of Baby Boomers.

And New South Wales will become the health boom capital of Australia, with 44 per cent of those from the state vowing to prioritise their health in the new year - higher than Victoria (39 per cent), Queensland (34 per cent), Western Australia (29 per cent) and South Australia (27 per cent).

But the findings also reveal there has been a jump in Aussies ditching New Year’s resolutions all together - up from 25.8 per cent in 2025 to 31.9 per cent in 2026.

The sad reality is that while we set these health and fitness goals with the best intentions, some people don’t stick to their plan if they have a cheat day or suffer a setback. I’m not a health guru but I’d say that’s pretty normal.

The good news is, for 13.7 million Australians who have extras health insurance, they could already be paying for services to aid their health goals.

Health insurance is more than just dental check-ups or optometrist appointments. You’d be surprised at the types of services available that can help you live a healthier lifestyle.

And you may already be paying for the service. While benefits vary between policies and health funds, you may be able to claim on things like gym memberships, lifestyle programs, dietitian consultations, remedial massage and more.

If you have an extras policy, see if you can access these services. Or if they’re important to you and you think they’ll help you on your health journey, compare your options and consider switching to or taking out a policy that offers them.

The research also found that 7.9 per cent of Australians said they would drink, smoke or vape less in 2026 - down slightly from 8.6 per cent in 2025. These can be expensive habits, so in addition to improving your overall health, kicking them could help boost your savings in 2026 too. If you were spending $80 a week on these habits every week, which isn’t hard if you’re going out with mates or winding down the week with work colleagues, it works out to be $4,160 over a year. That’s enough for an overseas holiday, a new laptop, phone or even an update of your wardrobe.

Other top resolutions Australians made in 2026 include:

Saving more money (35.3 per cent).

Going on a holiday (24.8 per cent).

Buying a new car (9.7 per cent).

Being more environmentally conscious (9.6 per cent).

Why Trump is controlling Venezuela

Check out the world’s top 10 countries with the biggest oil reserves, according to OPEC’s 2024 report. Venezuela leads, with Saudi Arabia and Iran not too far behind. It’s wild to see just how concentrated global oil really is!

Venezuela holds about 303 billion barrels of proven crude oil reserves, or 19.4 per cent of the global total, making it the world’s largest holder.

Saudi Arabia ranks second with 267 billion barrels (17.1 per cent), while Iran follows with 209 billion barrels (13.3 per cent). Together, the top three countries account for nearly half of global proven reserves.

Canada is the largest non-OPEC country, with 171 billion barrels (10.9 per cent), largely from oil sands. Iraq (145 billion barrels, 9.3 per cent), the UAE (113 billion barrels, 7.2 per cent) and Kuwait (102 billion barrels, 6.5 per cent) further underline the Middle East’s dominance. Russia (80 billion barrels, 5.1 per cent), Libya (48 billion barrels, 3.1%) and the United States (45 billion barrels, 2.9 per cent) complete the top 10.

In a nutshell:

Venezuela holds nearly one-fifth of global proven crude oil reserves, topping the global rankings.

The top three countries control almost half of the world’s oil reserves, highlighting high concentration.

OPEC members dominate the list, reinforcing their long-term influence over oil markets.

Canada leads non-OPEC producers, ranking fourth globally by reserves.

The United States ranks last among the top 10, highlighting the gap between production leadership and reserve size.

Explains recent news, don’t you think?

Have a great week, everyone.